Circle The Drain

Inflation – the act of inflating; the state of being inflated; sharp increase in the amount of money and credit causing advances in the price level – The New Webster Encyclopedic Dictionary Of The English Language (1971)

In the summer of 1885, amidst the cobblestone streets of Mannheim, Germany, Carl Benz, a pioneering inventor with an audacious vision, prepared for an unprecedented journey that would echo through the corridors of history. The Motorwagen, a mechanical marvel with three wheels and a combustion engine, was a testament to Carl's ingenuity. As he meticulously adjusted the levers and gears, Carl couldn't shake the excitement tinged with apprehension. He was about to unveil not just a vehicle but an epochal shift in human transportation.

The moment the key turned in the ignition, the Motorwagen grumbled to life, and Carl, holding the steering tiller with determination, set forth onto the winding streets. The primitive roads, riddled with imperfections, immediately tested the vehicle's suspension and the mettle of its driver. The distinct sounds of the engine echoed through the air, capturing the attention of Mannheim's residents, who gathered along the sidewalks to witness this mechanical spectacle. Horses startled, and pedestrians hastily made way for the unconventional creation, giving Carl a challenging yet exhilarating baptism for the Motorwagen.

The journey, however, was more than a mechanical demonstration. It was a public spectacle, drawing a mixture of bewilderment, skepticism, and awe from onlookers. The vehicle's unfamiliar appearance prompted whispers and discussions among the crowd, with some questioning the practicality of such a contraption. Carl, undeterred, navigated through the lively streets, showcasing not only the vehicle's capabilities but also his skill as a driver and the viability of his groundbreaking creation.

As the Motorwagen ventured farther, it faced unforeseen challenges. Mechanical glitches surfaced, causing intermittent pauses in the journey. Carl, displaying a resilience that mirrored the Industrial Revolution itself, tinkered with the contraption on the roadside, improvising solutions to keep the Motorwagen on its course. Each hiccup, far from being a setback, became a lesson learned and an opportunity for refinement.

Despite the challenges and uncertainties, the Motorwagen completed its inaugural journey, reaching a destination that transcended the physical distance covered that day. Carl Benz's ambitious drive marked not just the birth of the automobile but the dawn of a new era in transportation. Unbeknownst to him, the ripples from that historic drive would cascade through time, laying the foundation for an industry that would revolutionize the way people moved, connected, and explored the world.

As a child, I owned an audio cassette featuring the story of Carl Benz’s second drive from Mannheim to Pforzheim, which captivated my imagination. The hurdles he had to overcome to travel just 39 kilometers (24 miles) in 7-8 hours, fine-tuning the Motorwagen along the way, adjusting the machine, etc., left a lasting impression on me.

In today's context, it somewhat parallels the actions of central bankers who seek to 'fine-tune' the economy with interest rate policies. When the economy rapidly expands due to low interest rates, akin to a car descending a hill, the central bank applies the brakes by increasing rates.

Conversely, when the economy falters, resembling a car climbing a hill, the central bank presses on the gas, attempting to boost economic activity by lowering interest rates. Studying historical central bank hiking cycles reveals that central banks often tend to overdo it in one way or another.

In 2020, as the economy came to a sudden halt due to government policies, central banks injected money into the economy, funneling it through government spending, thereby elevating the inflation rate. In 2022, central banks began tapping the brakes to curb consumer price inflation. The question arises as to whether they might once again overdo it.

Since the summer, a substantial debate has unfolded regarding whether turmoil in the Middle East will lead to a surge in oil prices and, consequently, an increase in consumer prices. As consumer prices in the United States began to rise slightly in July, some financial analysts suggested another wave of inflation might already be in the making.

The introductory quote is from Webster’s dictionary of 1971. Since then, the meaning of the word 'inflation' in common usage has evolved:

1. : an act of inflating : the state of being inflated. 2. : a continual increase in the price of goods and services

This issue surfaced after an extended debate within the scientific community regarding whether the money supply truly wields as much influence on inflation as economists initially believed. Finally, in the 2010s, following years of quantitative easing that failed to manifest in consumer price inflation figures, many New Keynesian economists—the prevailing theory among macroeconomists—claimed victory. They saw it as evidence that the growth of the money supply does not predominantly trigger inflation.

While there has been a recent slight shift in their stance, they still resist the notion that the money supply is the primary driver of general price level increases. Advocates of Modern Monetary Theory go even further, asserting that rises in general consumer prices are simply the outcome of supply-driven factors, with money supply playing no significant role.

Now, as many inflation hawks predict the onset of a new inflationary wave, I believe it's an opportune moment to revisit the topic and assess the current state of financial markets.

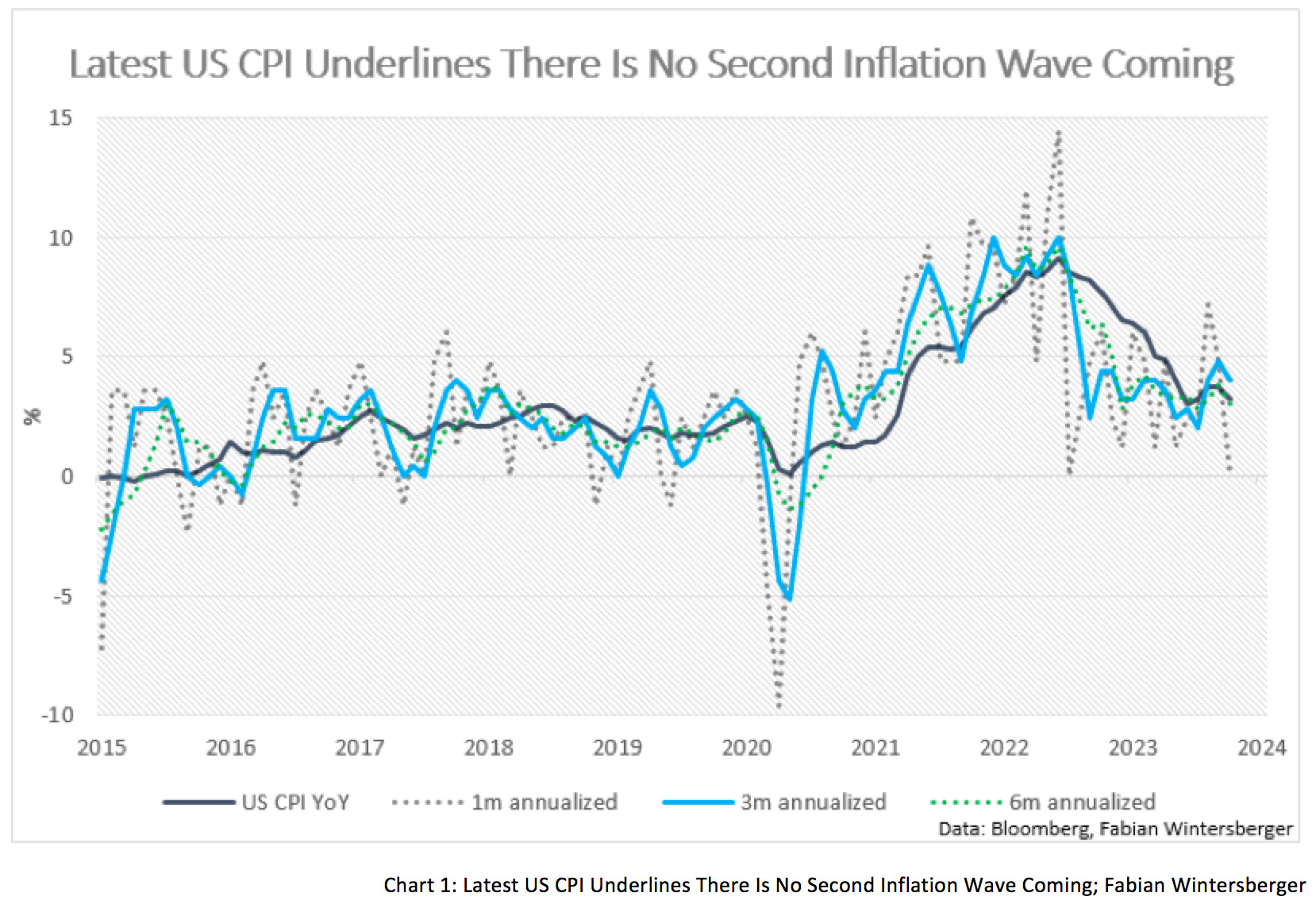

The October inflation figures brought disappointment for inflation hawks. Following an increase from 3% to 3.7% year-over-year between June and September, many anticipated continuing the upward trend. However, with prices remaining flat month-over-month, consumer prices failed to rise further and dropped to 3.2% year-over-year—more than expected. Both the 3-month and 6-month annualized CPI also experienced a decline.

When examining Powell's preferred 'Super Core' (Core Services Less Housing), it decreased from 3.95% to 3.91%. Core CPI also experienced a slight decrease, moving from 4.1% to 4%.

As a result, markets saw a strong rally, particularly the Russell 2000, which I recommended as a short-term speculative buy last week. It is up approximately 5.5%, while the S&P and the Nasdaq are up around 2.25% (as of Wednesday's close). Bonds also rallied, causing the 10-year treasury yield to drop from 4.63% to 4.49%.

Some inflation hawks dismissed these numbers as 'phony' due to an adjustment in healthcare. Nevertheless, the PPI numbers on the following day underscored the ongoing disinflationary trend. Producer prices came in cooler than expected at only 1.3% year-over-year and down 0.5% month-over-month.

It shouldn't be surprising that consumer prices continue to disinflate, meaning the rate of change of price increases is slowing. After all, as Milton Friedman famously said, inflation is a monetary phenomenon, and the money supply is already shrinking, pointing toward potential deflation in 2024.

However, as mentioned earlier, the idea that rising consumer prices should be referred to as 'price inflation' because they are merely a consequence of 'inflation' (a rise in the quantity of money not accompanied by a similar rise in the quantity of goods produced) is debated. Furthermore, an increase in the quantity of money might not impact consumer prices as much as other prices.

Returning to the claim that the QE era proves that money supply growth doesn't lead to (consumer price) inflation, one must examine how QE works and how it may or may not affect consumer prices. QE involves the central bank buying long-duration bonds and exchanging them for 'bank reserves'—digital money.

When the central bank buys a bond, it pays the bondholder money. During the Great Financial Crisis, the Fed strengthened banks' balance sheets by purchasing MBS at par instead of paying the market value. This action doesn't directly impact consumer prices; the effect depends on what the bond seller does with the extra cash.

If the seller is a bank, it can either invest it in other bonds or use it as a reserve to lend money to businesses, boosting economic activity and demand for commodities, goods, and services. If the seller is a pension fund, it will likely reinvest the money into other bonds and stocks, leading to further price increases in financial assets. In the case of a private investor/business, the money can be used to buy goods and services or reinvested in other financial assets.

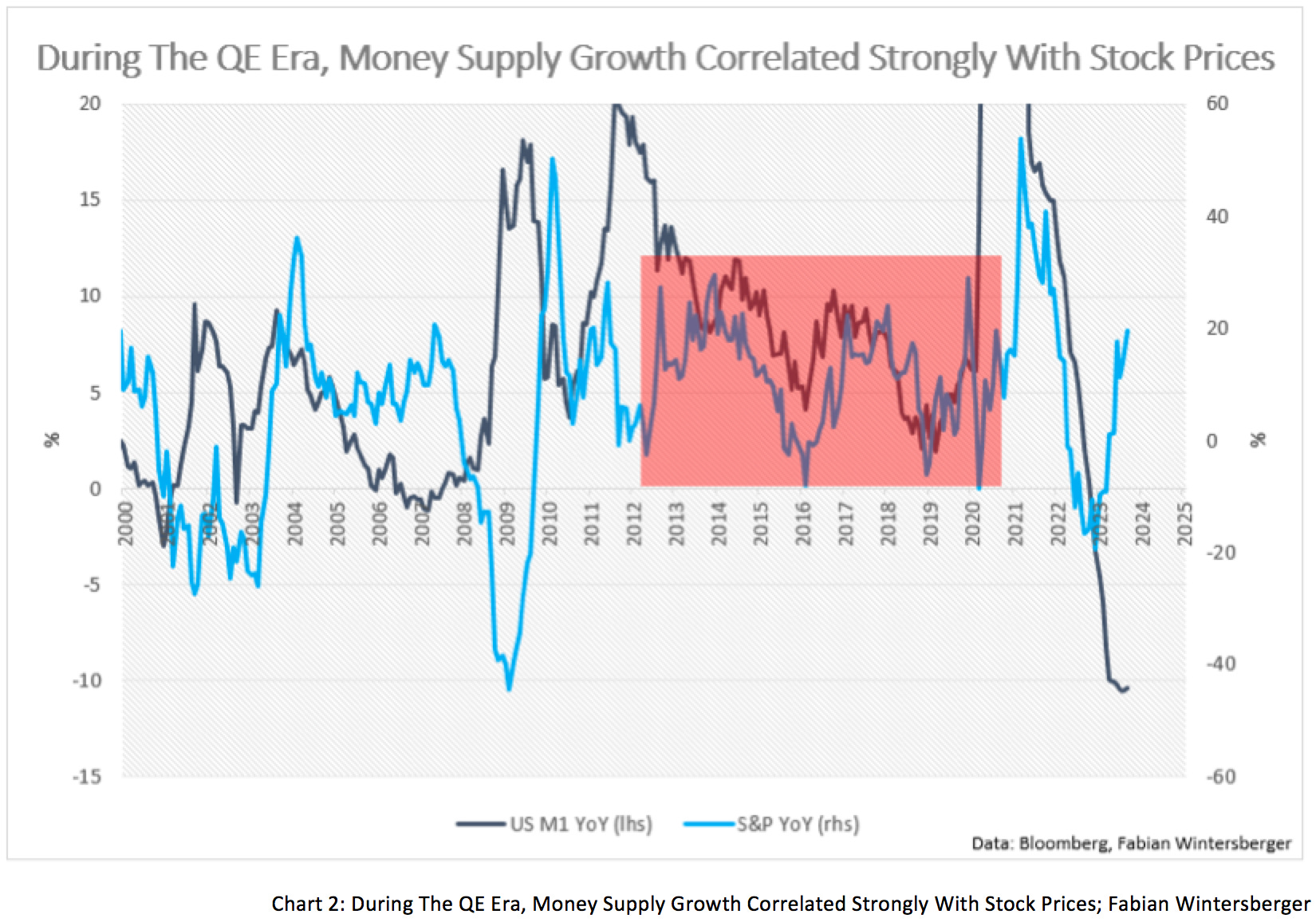

The primary beneficiaries of QE during the 2010s were banks, hedge funds, and pension funds, the largest holders. These entities reinvested a significant portion into financial markets, and as a result, consumer price inflation remained subdued and did not rise. The correlation between stock prices and money supply during the QE era reflects this.

While a significant increase in the money supply may not immediately result in a sharp rise in consumer price inflation, it represents an inflationary pressure that could potentially manifest as higher consumer prices in the future. Currently, the injected money remains predominantly confined to financial markets, showing no indication of an imminent shift toward the real economy.

While the Fed has been cautious in purchasing corporate bonds, the ECB has engaged in such purchases. However, this alone does not guarantee an automatic escalation of consumer prices. If the original bondholders utilize the newly created money to invest in other financial assets, it will merely contribute to the inflation of asset prices.

Nevertheless, it's crucial to acknowledge that heightened demand for bonds tends to drive bond prices upward, subsequently lowering interest rates. This, in turn, enables companies to borrow money at more favorable rates. However, even with this advantage, there is no certainty that the increased borrowing capacity for businesses will inevitably translate into rising consumer prices.

The 2010s witnessed the prevalence of "stock buybacks," where companies issued debt to repurchase their stocks, boosting stock prices and benefiting CEOs and shareholders through bonuses and dividends. Given that these individuals mainly belong to higher-income groups, the impact on consumer prices will likely remain limited, as they are more inclined to reinvest the money in other financial assets.

However, it's essential to consider an alternate scenario where artificially lowered interest rates could contribute to inflation. Declining interest rates imply a reduction in the cost of capital, encouraging businesses to borrow from banks or capital markets and invest in real economic activities, thereby artificially boosting demand for goods and services and driving prices higher.

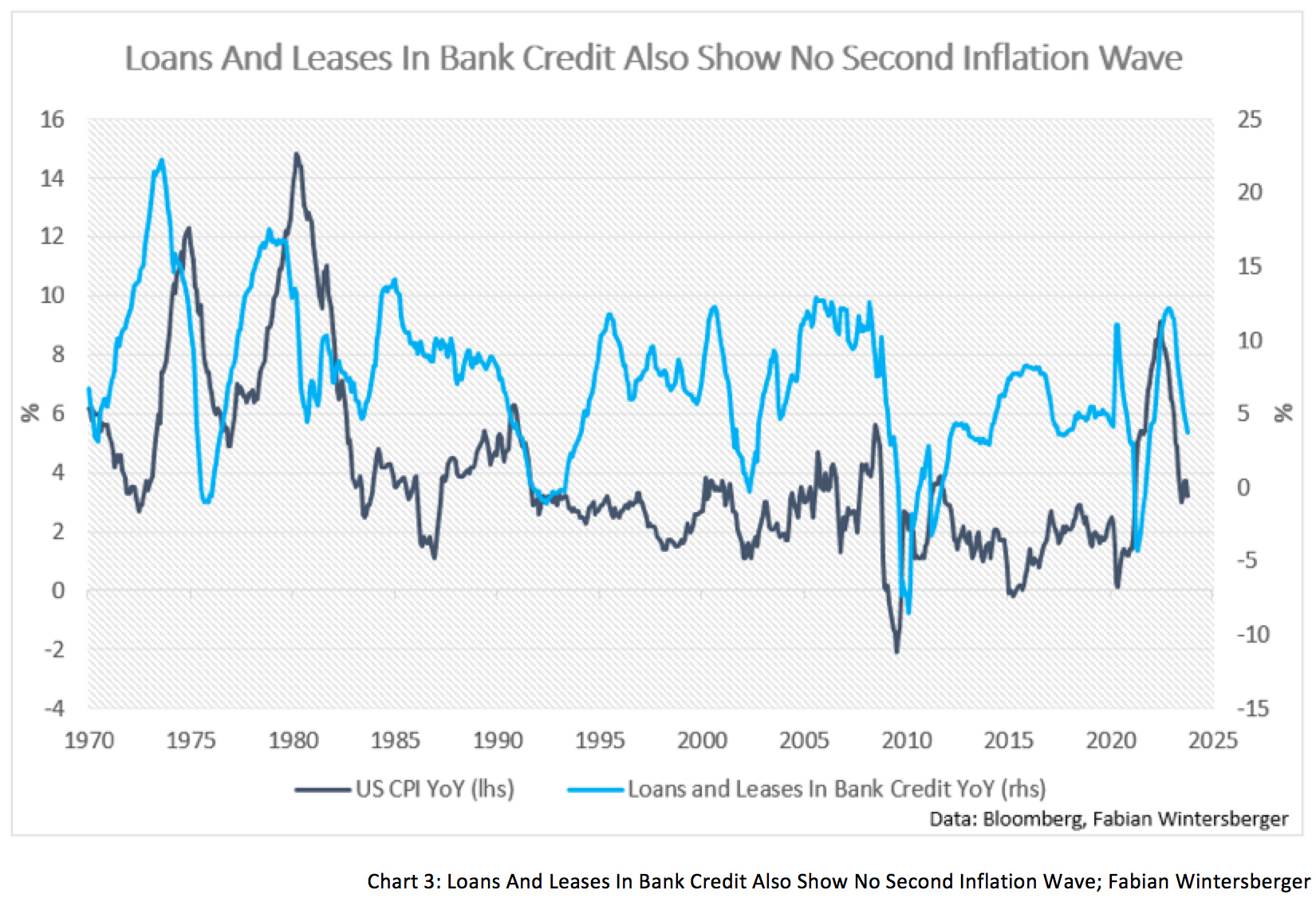

If the money indeed flows into the real economy, it stimulates demand and, subsequently, prices. While inflation experienced an uptick in 2021, bank credit for loans and leases also significantly increased. However, as the Federal Reserve raised interest rates, the cost of capital rose, leading to a slowdown in bank lending, returning to pre-COVID levels.

Governments, on the other hand, typically inject the funds they borrow directly into the real economy. This action boosts demand, subsequently affecting consumer goods and services prices. This explains why the bond-buying initiatives of central banks during the COVID-19 pandemic yielded significantly different outcomes than those in the 2010s.

During the pandemic, the government, while simultaneously impeding the production of goods and services, acquired substantial amounts of funds at favorable interest rates. These funds were then distributed to the public through stimulus checks, resulting in increased demand for various economic sectors, particularly in stay-at-home goods. This surge in demand consequently led to higher prices and increased income for individuals involved in these sectors.

As the economy reopened and more stimulus funds were distributed, it fueled increased demand. Meanwhile, financial market participants, anticipating the continuation of ZIRP, eagerly bought the bonds the Fed was acquiring on the secondary market, thereby boosting the money supply. Despite financial actors ending up with the same amount of money, the government found itself with more cash to spend.

However, the money supply remains unchanged if the Fed refrains from purchasing bonds on the secondary market. In fact, as more debt is paid down, the money supply contracts. Assuming the quantity of goods and services produced remains constant, price inflation cannot be.

Some have pointed to the recent rise in oil prices to argue that inflation will increase. However, this perspective tends to confuse an increase in the general price level with changes in relative prices. The fact that the price of one commodity rises does not necessarily mean a simultaneous increase in all prices.

Another illustrative chart comes from the latest NFIB report, indicating that a growing number of small businesses are either planning to raise prices or have already done so. Despite these actions, consumer prices as a whole experienced a decline in October.

As the money supply contracts, the general price level cannot rise. If prices for goods and services produced by small businesses increase, prices for other goods and services must decline if the same quantity of goods and services is being purchased. Rises in the general price level can only be temporary in such a scenario, as it will impact the quantity of goods sold, leading to a return of some prices to their equilibrium rate.

Consider a situation where raw material prices increase universally while workers demand higher wages. If the cost of raw materials doesn't decrease, businesses may eventually have to reduce their workforce unless they accept lower wages. This would augment the supply of workers in the market, driving wages down and bringing the price level back to its previous state. On the contrary, if raw material prices somehow decrease, wage rates can remain constant.

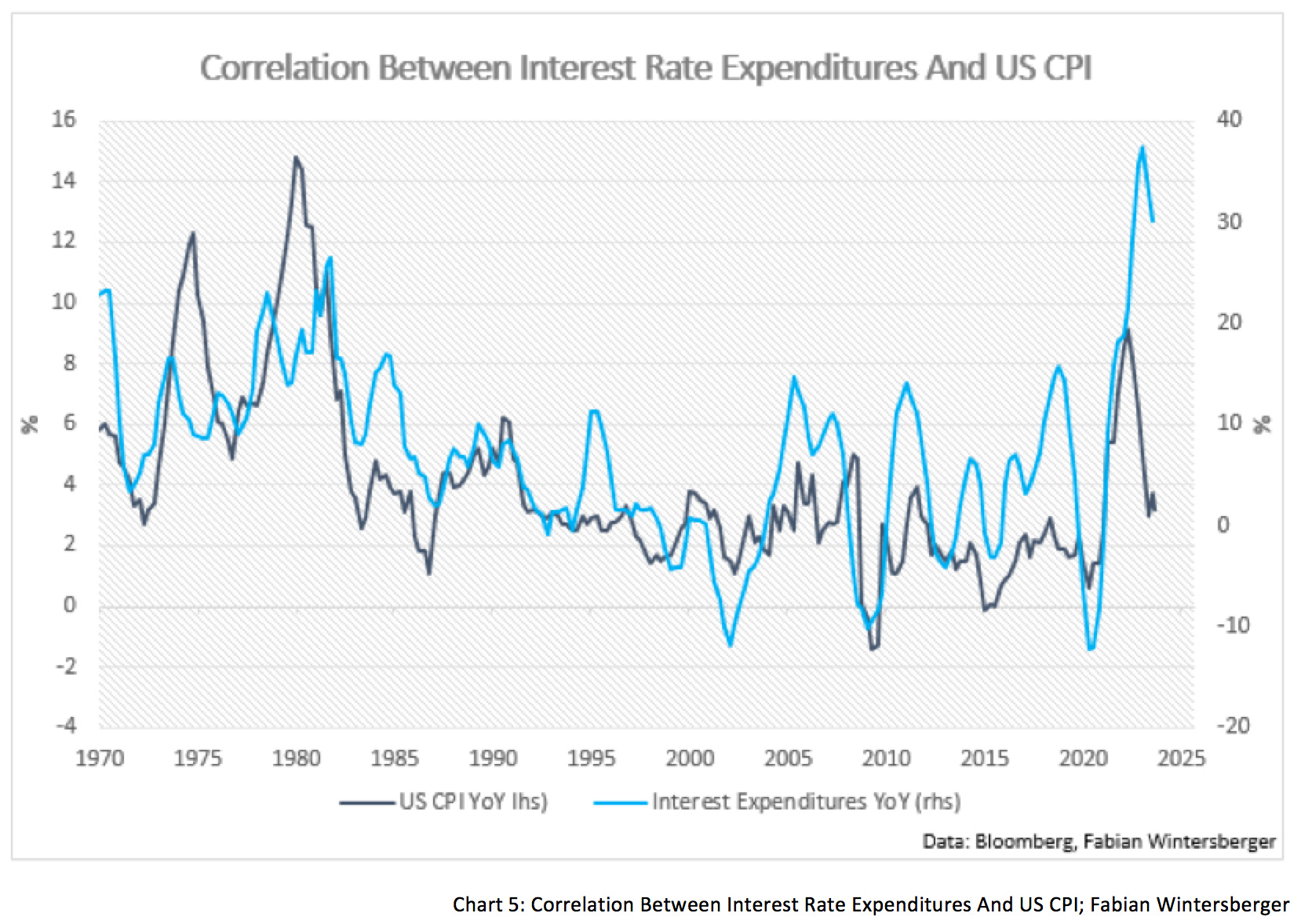

There's an argument that higher interest rate payments from the government could fuel inflation. While many people have refinanced their homes at a low rate and can now invest their savings in financial assets at a higher yield, resulting in higher income, it doesn't necessarily translate to increased inflation.

Since many recipients of interest rate payments are wealthier, they are more likely to reinvest in other financial assets rather than use them for consumption. While some may increase their consumption, slowing the decline in the rate of change, the correlation between CPI and government interest rate expenditures, as shown in Chart 5, is not strong enough to offset another potential inflation wave. It's more accurate to say that higher interest rate income is a consequence of higher inflation, not the other way around.

The question of whether the deficit is unsustainable essentially revolves around the future need for the Fed to monetize the debt, bringing it down to manageable levels. However, this isn't the driving force behind financial markets in the upcoming months; thus, a second wave of inflation is unlikely.

The only scenarios where CPI might pick up speed despite a declining money supply would involve a significant drop in supply or a sharp decrease in currency demand/financial assets coupled with an increase in the demand for goods and services. This would be the so-called "Endgame" that many people discuss, but it remains distant and may never materialize.

It's more probable that the aggressive tightening by central banks after an extended period of loose monetary policy will lead to an economic contraction. While certain factors have prolonged the expansion, an impending non-linear event is on the horizon. While my current projection places this event later in Q4, the implications remain consistent even if it takes one to two quarters longer.

Bonds become increasingly attractive as we approach the end of the economic cycle and the economy heads towards a significant slowdown. However, the current market dynamics are unique, and I would still lean towards the short end rather than the long end or prefer call spreads over directional buying.

The stock market may continue to rally in this cycle stage, with market participants initially celebrating poor economic data as a signal that rate hikes are over and later anticipating more cuts than expected. However, this trend usually persists until stocks struggle to reach new highs, while bond yields start to fall—a signal to adopt a more defensive stance.

The EUR/USD exchange rate unfolded as anticipated last week, with the Euro gaining substantial ground against the dollar. The question is whether the move has more room to grow or if the spike has already peaked. A cautious risk reduction might be prudent at this juncture.

Looking ahead, it appears that inflation hawks will face challenges, and the same might be true for adherents of the Goldilocks scenario. However, this doesn't necessarily translate into an opportune moment to rush into bearish bets on the US stock market.

Long ago, I highlighted that inflation would decrease for the wrong reasons, urging careful attention. The money supply remains the most reliable guide to gauge the mid-term trajectory of consumer price inflation.

Inflation will likely come back when central banks revert to expansive policies. Nevertheless, there's an increasing openness to the idea that Jerome Powell might surprise everyone and attempt to sustain economic rebalancing for as long as possible. On the other hand, other central banks, like the ECB and the BoE, will likely continue to Circle The Drain.

If we really wanna change, we gotta learn from our mistakes

Can we start over, start over?

With a past we can't erase, and a stain to every name

Will we find closure or circle the drain?Wage War – Circle The Drain

Have a great weekend!

Fabian Wintersberger

Thank you for taking the time to read! If you enjoy my writing, you can subscribe to receive each post directly in your inbox. Additionally, sharing it on social media or giving the post a thumbs-up would be greatly appreciated!

(Please note that all posts reflect my personal opinions and do not represent the views of any individuals, institutions, or organizations I may or may not be professionally or personally affiliated with. They do not constitute investment advice, and my perspective may change in response to evolving facts.)