Calm Before The Storm

While the times have been somewhat turbulent in financial markets throughout the summer, one did not spot any difference in the real world. This summer has been like every other, and no signs that worrisome times are on the horizon: hotels were booked, restaurants filled, hiking routes and lakes full of people.

The calm before the world departs into unknown territories? It is hard for me to answer this question. Still, at least I can say that the topics of inflation, the war in Ukraine, and the looming energy crisis were topics everyone discussed only slightly.

However, summer is coming to an end, and all those topics will become more discussed in the broader public. So, how did we get there? In February, Russia invaded Ukraine, and the West decided to support Ukraine in both ways entirely: they sent weapons and war machinery and imposed extreme sanctions on Russia. The ruble tanked, and people thought that the Russian economy stood on the brink of collapse.

But Russia somehow could prevent the economy from collapsing. They stabilized the ruble by demanding payments in rubles for gas and raising interest rates. And Putin shot back by lowering the gas supply to Europe. During the summer, European politicians raised concerns that there could be problems with the energy supply in the coming winter. So, the EU Commission planned to secure the energy supply in the coming winter and after that.

EU-member states now have to fill up their gas storage by 80% until November this year (90% in the coming years). That agreement led to a significant increase in demand in the European natural gas market, and governments bought as much gas as they could, thus driving up the price.

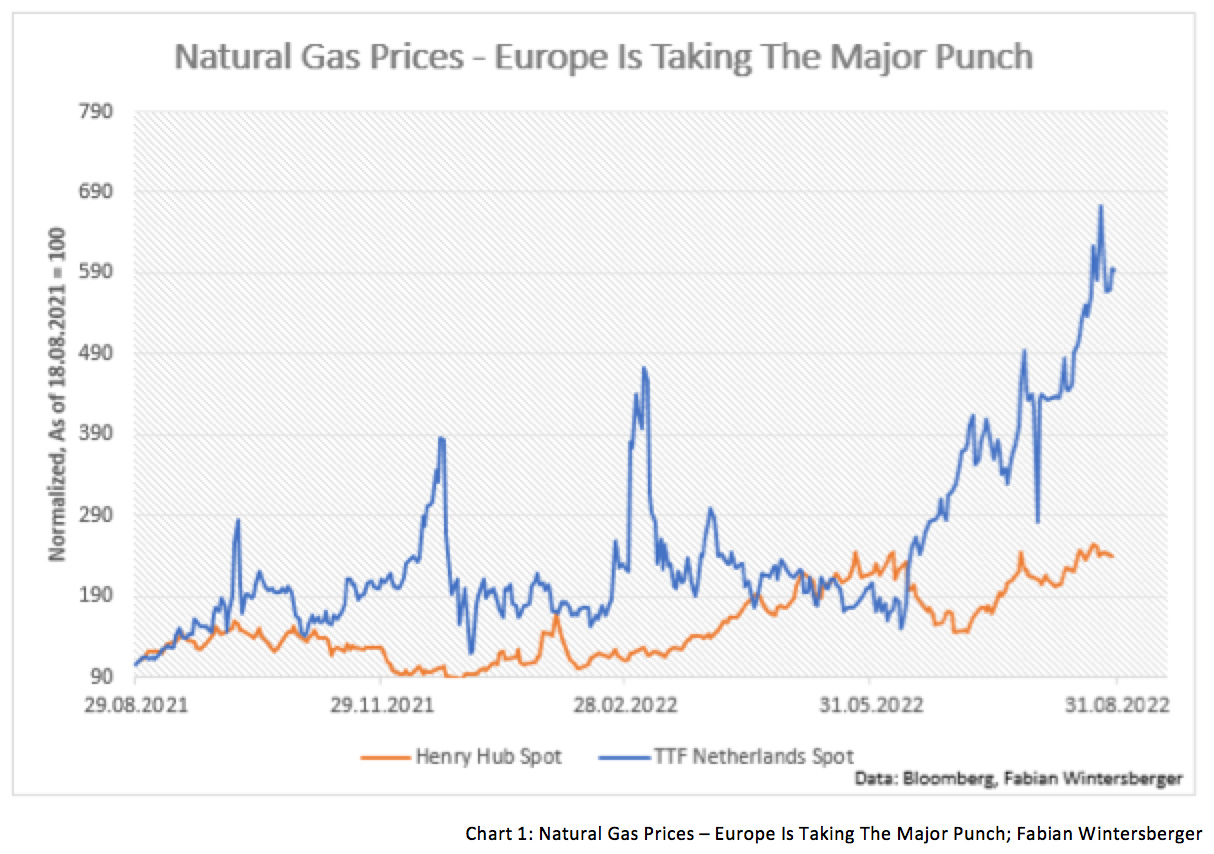

Although gas prices rose all around the globe, Chart 1 shows that Europe is taking the major punch. While natural gas prices rose ‘only’ by 140% in the United States, they rose by 500 % in Europe.

As a result, European base load prices also exploded to the upside. For example, the German baseload 1y forward spiked above 1,000 euros per megawatt hour. Many businesses feel pressured because they cannot easily pass the costs to consumers. Ursula von der Leyen announced that the EU would have an emergency meeting next week to address the energy market. Or, as the Czech minister of trade said: The energy market is not functioning anymore.

Although gas storage is well filled all around Europe, it is not so far-fetched to expect energy rationings this winter. As Alexander Stahel noted, the vast majority of EU countries need three times more gas than they have storage, which means that gas consumption would need to fall at least a third to avoid energy fallouts.

A big lever to save gas would be industrial consumption. However, one would need to close many parts of production, leading to an increase in unemployment. While many say this would lead to a deflationary shock, I tend to disagree and argue that such policies would put more fuel to the inflation fire. The unemployed would receive unemployment benefits (and possibly other transfers like the Austrian Teuerungsbonus) while supply is falling. If supply is falling faster than demand, inflation goes up. Additionally, the falling exchange rate of the euro has made imports more expensive. This week, the Estonian central banker Madis Muller said that the ECB would discuss a 75bps rate hike at its September meeting. My odds would be that the hawks will have the upper hand against the doves in the governing council.

From the Fed, the ECB cannot expect any help either. Robust US consumer data and a still low unemployment rate give the Fed more firepower for rate hikes. At Jackson Hole, Powell signaled to markets that the Fed would keep tightening until inflation was under control. History tells us not to loosen too soon, Powell said.

Will a Federal Funds Rate of 4% do the job, as markets expect? I remain skeptical because current inflation rates are still a result of fiscal stimulus and supply chain problems. Energy inflation is just starting to spread throughout the economy. And they are not only affecting Europe because a ban on Russian energy will lead to higher demand for products from other exporting countries and thus higher domestic prices.

Energy is just machine food. If the price of energy rises, the cost of everything increases. Higher energy prices mean higher production costs and logistic costs. As long as unemployment stays low, central banks have no incentive to loosen monetary policy again. It would be too soon anyway, and it would not help to fight the inflation wave coming from the energy markets. Commodity prices recently turned north again, suggesting that inflation has not peaked.

Many say that the situation is similar to the inflationary waves of the 1970s, where the Yom Kippur war and the following oil embargo of Arab countries caused an energy price shock and skyrocketing inflation. However, I would add that inflation is already close to 10%, 50% higher than before the Yom Kippur war.

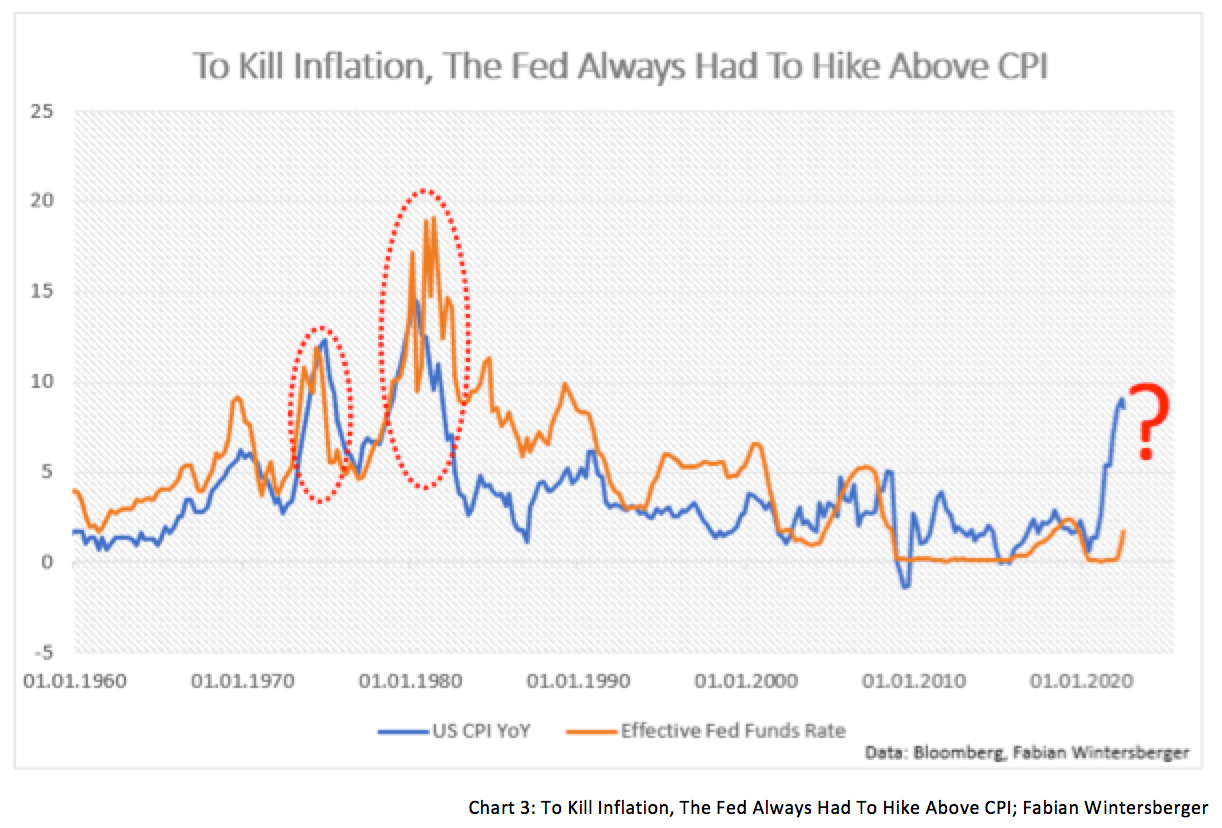

Powell referenced Paul Volcker several times during his Jackson Hole speech. Volcker brought inflation back down to earth when he became Fed chair. Many commentators say that Powell wants to be Volcker 2.0 instead of a new version of Arthur Burns. Burns was Fed chair from 1970 to 1978 and is well known for pivoting prematurely and failing to fight inflation sustainably.

Under Burns, the Fed pivoted, and the market still expects that Powell will do the same. Currently, the market expects will hike rates up to 4% and then pauses for a year. Back in 1974, pivoting meant hiking rates to the level of inflation. That leads to whether the market is correct to assume that 4% will be the ceiling. Will inflation fall back to 4% until year-end? Hard to say, but problems in the energy markets are just starting. I assume that central banks need to hike rates much higher if they want to fight inflation, which is higher than the market is currently expecting.

During the last decade, the impression was that the central bank’s main focus was rising asset prices. And while the stock market has lost some gains from 2021, all indices around the globe are still at levels where they have been at the end of 2020. That means that the everything bubble is still alive and has not popped yet, which gives central banks more room to raise rates.

Additionally, there is quantitative tightening. On the one hand, by not reinvesting the income of matured treasuries, on the other hand by actively selling bonds into the market. Rising supply and falling demand by central banks translate into falling bond prices and, thus, higher yields.

The yield curve will probably flatten further and get more inverse. However, I expect that the curve will also shift upwards. In the 1970s, the spread between 2y and 10y treasuries inverted by about 200bps. That means that if 10y yields remain at current levels (about 3%), the Fed would need to hike to 5%. If inflation rises further, the Fed would need to hike, even more, leading to higher long-term rates.

If the West continues to ban Russian energy, cheap energy will be a thing of the past. Costs for businesses will rise. Further, since oil and gas consumption is expected to increase in the coming years, the result will be additional inflation pressures.

I want to add that there also are other price pressures than energy. Since the pandemic, the EU and the US have announced that they plan to re-shore critical industries and bring production back home from the far east. In the same way, off-shoring in the 1980s was deflationary; such policies would be inflationary.

Another factor is that the supply of workers is likely to decrease in the coming years. The baby-boomer generation is ready for retirement, causing upward pressure on wage rates. And if all this was not enough, governments plan to put more regulation into legislation which would also be inflationary because it raises the cost of doing business if businesses do not outsource production or close.

In my opinion, the great stagflation has just started, and as a result, central banks have to raise rates much more than the market anticipates. Markets still expect that the coming recession will push inflation back down. However, this will not happen if inflationary forces are more substantial than deflationary ones.

Now it gets a bit tricky. The assumption that central banks can easily hike rates as they did back in the 1970s has a catch. Take the United States as an example. In the 1970s, US debt/GDP was 30%; nowadays, it is above 120%. And this is just government debt; things do not look better on the business level. Additionally, loose monetary policy in the past decade has led to an increase in companies that could not handle such high rates.

I should add that the Fed has more possibilities than the ECB because, different than the euro area, the United States is a homogeneous economic area. Therfore I expect that the euro will continue to fall against the dollar if the current environment persists.

That means the ECB will reach its limit much sooner than the Fed in an environment of rising interest rates. Nevertheless, the US will also get to a point where the rise in rates cannot be handled anymore. But if the dollar remains stronger compared to other currencies, this would be deflationary because the US can import more goods at a lower cost. I would not be surprised if we see falling inflation rates in the United States (energy net exporter) while inflation is still rising in the Eurozone (energy net importers).

Still, investors need to understand that inflation will not go back to central bank targets in Europe or the US. To achieve that, governments would need to cut back on spending drastically, deregulate, and increase the energy supply to bring costs back down. However, the green transition will lead to the opposite, at least in the short and medium term. Prices for commodities to produce PV and wind wheels will rise because of rising demand. Not to mention that it will be mainly the Chinese who profit because Chinese producers have a comparative advantage against European producers.

Now we are back to the most crucial topic these days, energy. As the US will increase its SPR in the coming fall, oil prices are poised to rise even more, significantly, if tensions in Lybia are growing again. Another problem for Europe is that the US may put their interests above one of their allies, as in the recent letter from US secretary of energy Jennifer Granholm to US refiners. She asked them to lower exports to increase domestic storage levels in the letter.

Additionally, the situation will not improve in the natural gas market, even if Russia keeps sending as much gas as it currently does. Polen, which does not receive Russian gas because it refused to pay in rubles, is in trouble because of problems with the Baltic Pipeline, as Handelsblatt reported this week.

It is hard to imagine that Europe will be able to stay hard against Russia, despite that it should be done from a moral point of view. The public will pressure governments at some point because of non-affordable energy costs and probably because of skyrocketing unemployment. Already many producers are scaling back production, including fertilizer producer Yara and bakeries, for example. While this is still far away for Europe, it looks as if Japan is already reconsidering. As Reuters reports,

Japan's biggest city gas supplier Tokyo Gas Co Ltd has signed a long-term contract with a new Russian operator of Sakhalin-2 energy project to buy liquefied natural gas (LNG), a spokesperson for the Japanese company said on Tuesday.

European policymakers may see soon that people will not be willing to suffer endlessly. In the end, policymakers have to win domestic elections, even though most are still years away. One could easily say that the letter from Jennifer Granholm is just populism ahead of the mid-term elections. Still, I think this underlines the argument that the US will let Europe down if things get serious in the United States.

Such a scenario would be even more inflationary for the euro area, and the ECB would need to act even more restrictive. A central bank pivot is far away, which means that a potential storm is brewing, not only in Europe but also in markets. Things could get worse, not only economically but politically too.

As Light The Torch sing in their song Calm Before The Storm:

The nights are getting colder

The days are growing long

And you do not know

What you're fighting for

Come back to where you started

Come back where you belong

And I won't be your

Calm before the storm

I wish you a splendid weekend!

Fabian Wintersberger

Thank you for reading! You can subscribe and get every post directly into your inbox if you like what I write. Also, it would be fantastic if you shared it on social media or liked the post!

(All posts are my personal opinion only and do not represent those of people, institutions, or organizations that the owner may or may not be associated with in a professional or personal capacity.)