Breaking The Mirror

Asset Inflation, Credit Expansion And The Fed's Dilemma

The artificial boom is not prosperity, but the deceptive appearance of good business.— Ludwig von Mises

It’s been quite an eventful week since my last report. We got the Nonfarm Payrolls Report and US inflation data for April, and to sum it up, the Fed is in a tough spot when it comes to delivering rate cuts for the President. The market increasingly prices in rate hikes, but I’m not so sure about that and will give reasons later.

Nevertheless, there’s still a ceasefire/war between Iran and the United States going on. The Strait of Hormuz remains closed and continues to cut off oil supply from the market. Interestingly, Goldman Sachs recently published a report estimating that the global damage from the closure of the Strait of Hormuz will remain “moderate.” The bank assumes that the rise in oil prices is coming to an end, with expectations that oil might ease toward $90/barrel by year-end.

Maybe the Xi-Trump meeting this week will lead to an improvement in the situation, as Trump expects China to put some pressure on Iran regarding the Strait. Whether that will actually happen remains to be seen (you probably know when the report comes out, as it is written on Wednesday due to Thursday’s holiday).

The US Labor Market Remains Strong

The April payrolls report suggests that the US labor market remains considerably more resilient than many expected despite the inflationary shock caused by the Iran war. Nonfarm payrolls rose by 115,000 for a second consecutive month above 100,000, while the unemployment rate remained stable at 4.3%. Hiring broadened across several sectors, especially healthcare, transportation, warehousing, and retail, indicating that labor demand is stabilizing after a weak 2025. The report reinforces the view that the US economy has not yet entered the kind of labor-market deterioration that would normally force the Fed into aggressive rate cuts.

At the same time, the details beneath the headline figures were more mixed. Labor-force participation fell to its lowest level since 2021, broader unemployment measures increased, youth unemployment rose sharply, and the household survey continued to show weakness in employment. While wage growth remained relatively contained at 3.6% YoY, average weekly hours increased, supporting household incomes for now. The divergence between strong payroll growth and weaker household survey indicators suggests the labor market may not be as strong as the headline numbers imply, though it remains far from recessionary territory.

For markets and the Fed, the report complicates the policy outlook considerably. The resilience of hiring, combined with rising inflation pressures from higher energy prices, reduces the urgency for rate cuts and may even strengthen expectations for additional tightening. At the same time, ongoing geopolitical uncertainty and weakening consumer sentiment raise the risk that current strength could fade later in the year.

To sum it up, the data reinforces a broader dilemma facing the Fed: inflationary pressures remain elevated while the economy continues to avoid the clear slowdown that would justify easier monetary policy. Albeit one can theoretically debate whether that reflects a strong labor market, I think the report clearly showed that the labor market remains far away from justifying a looser monetary policy stance.

Furthermore, I don’t think the rise in metrics such as youth unemployment poses a danger to the overall economy. Income growth might be slowing, but that leaves out the increase in “paper wealth” from stock market gains. That might not affect the lower-wealth cohorts, but it supports the borrowing capacity of the higher-wealth cohorts that increasingly drive US consumption. Additionally, the rise in inflation will likely play into their hands, as it supports asset prices and further lowers the real debt burden of fixed-rate borrowings like mortgages.

US Inflation Is Rising But The Fed Might Not Hike

US inflation accelerated further in April as the economic effects of the Iran war increasingly spilled into consumer prices. Headline CPI rose 3.8% YoY, the highest level since 2023, driven primarily by surging gasoline prices, rising grocery costs, and higher rents. Energy prices continued to ripple through the economy, lifting transportation costs, airfares, and hotel prices, while food inflation accelerated sharply as higher fertilizer and shipping costs fed into supply chains. At the same time, real wages fell for the first time in three years, suggesting that households are increasingly struggling to keep up with rising living costs.

Nevertheless, the report also contained signs that underlying inflation dynamics may not be as strong as the headline numbers suggest. Part of the sharp increase in shelter inflation was distorted by statistical effects related to the 2025 government shutdown, while core goods prices remained relatively subdued despite tariffs and higher fuel costs.

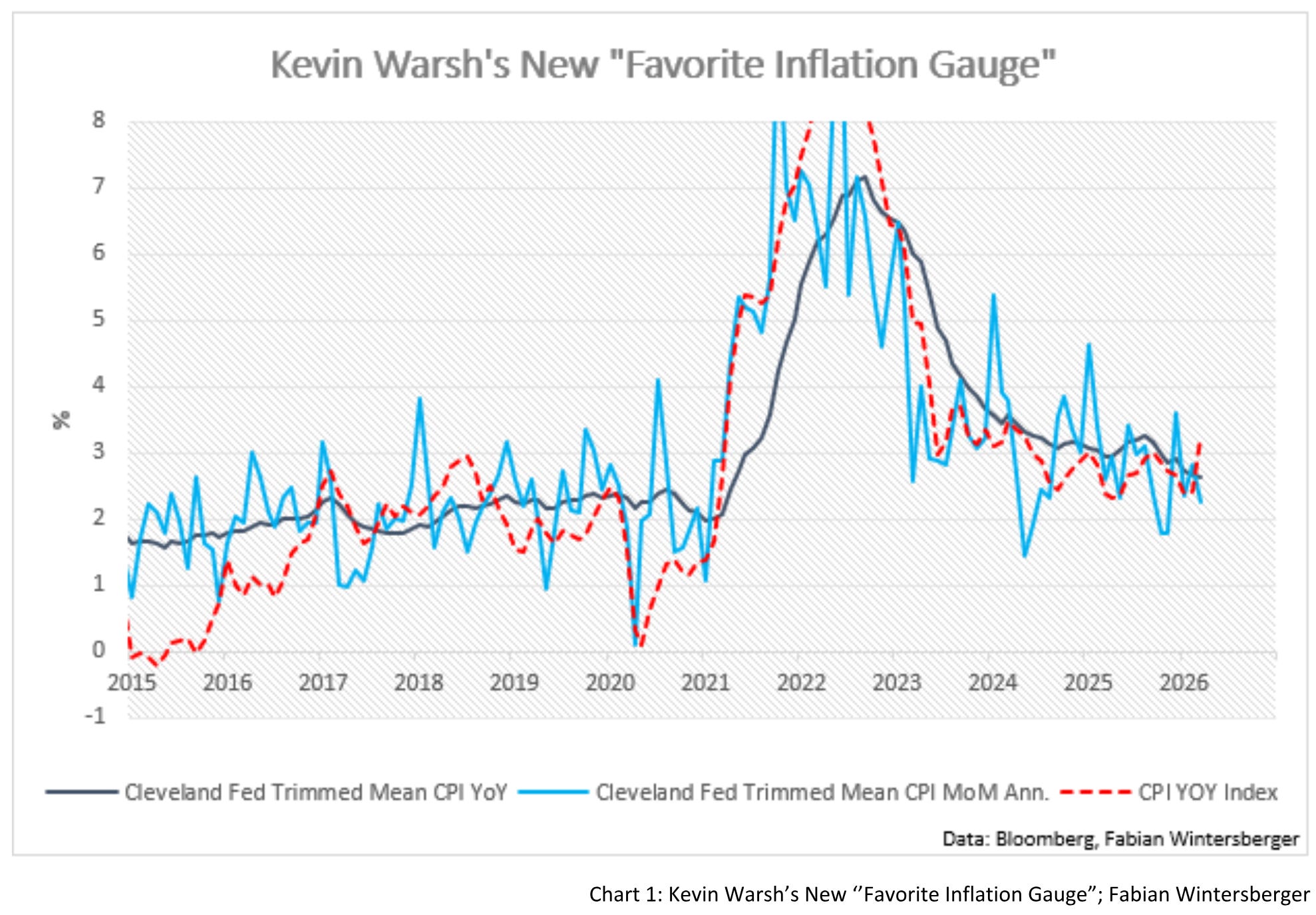

Combined with the far-from-recessionary labor market, it’s obvious that the data is not on the side of newly elected Fed Chair Kevin Warsh when it comes to fulfilling Trump’s hopes for rate cuts. However, during his hearing, Warsh already emphasized a potential workaround for that.

In the hearing, he insinuated that “trimmed mean inflation” is a preferable metric to “evaluate the underlying, generalized change in prices in the economy.” That metric, which excludes the top and bottom 8% of price changes to cut out outliers, is currently running roughly 1 percentage point below the official CPI number.

With this new “favorite inflation gauge,” one can justify keeping interest rates steady for longer, especially as long as the effects of inflation remain statistically concentrated in a few categories, such as energy and food. It might or might not be that inflation spreads further into other categories. If it doesn’t, I see a possibility that the Warsh-FOMC will not follow the market and raise interest rates.

Whether it will cut despite the data remains a different question, and I don’t think it is as important as many believe. My reasoning here is that rising inflation benefits debtors, while a large share of US consumption remains debt-financed. Further, and as noted in the beginning, inflation increasingly feeds into asset prices as well, and mostly much more than into consumer prices. That means that asset holders will effectively be “overcompensated” for the rise in CPI. That spread can then be used to increase borrowings and keep consumption or asset purchases going for longer.

Holding interest rates steady in such an environment already translates into a loosening of financial conditions. I think when Trump talked about rate cuts, he was more or less referring to loosening financial conditions to keep asset prices elevated and maintain room for debtors to continue spending.

Additionally, the government’s deficit also benefits from inflation and steady interest rates. A rise in long-term interest rates might not be as favorable as a decline, but as we know, Trump may still be able to jawbone the market for some time. The US Treasury, on the other hand, has already shifted much of its borrowing needs toward Treasury bills anyway.

That refinancing structure is also a headwind for long-term interest rates by lowering supply, while simultaneously mitigating the impact of higher refinancing costs. In the short term, I think this remains supportive for the economy, especially since Trump’s tax cuts also help keep profits elevated while dampening some of the upward pressure on prices.

In my view, Trump is currently trying to keep the system afloat at all costs. As long as these policies help sustain economic momentum, he will likely not bother much with the potentially dangerous side effects. Money continues to be printed and fuel economic activity until the distortions become visible to the broader public.

Inflation usually runs in three stages, as Ludwig von Mises once described. While his framework may appear somewhat outdated today, I have slightly adapted it to frame the current US economy. In stage one, consumers continue buying despite higher prices because their intuition tells them that rising asset prices have made them wealthier. More expensive purchases are delayed in the hope that income and wealth growth will eventually outpace inflation.

The second stage begins when people start pulling consumption forward because they expect inflation to continue. Cars, furniture and electronics get replaced sooner because expectations shift toward inflation becoming the new norm. As long as asset prices continue to appreciate, this dynamic remains manageable for the wealth cohorts driving overall economic activity.

I’ll skip the third stage — a complete collapse in confidence in the currency and panic buying — because I don’t think it is a feasible scenario for the United States. However, stage two can still be dangerous because looser financial conditions also affect businesses' long-term borrowing decisions. Rising inflation expectations push investors to demand higher compensation for lending, which drives interest rates higher.

If interest rates rise further as inflation worsens, and macro data increasingly point in that direction, with government spending, money printing, lending, and credit expansion continuing to fuel an artificial boom on top of an already existing boom, then the US may approach a tipping point.

Borrowing would increasingly be pulled forward to secure lower financing costs before rates rise further, pushing credit demand even higher while simultaneously feeding inflation through stronger real economica activity. More people are employed to complete projects that might otherwise have started much later.

At some point, stock market gains flatten despite inflation continuing to rise because new buying of financial assets slows while real-economic investment accelerates. Inflation rises further until public pressure becomes too strong and the Fed is eventually forced to react. When the Fed finally raises interest rates, the contraction begins, and markets must adjust to the new reality. Stocks fall, the economy slows and neither Trump nor the Fed can easily stop the adjustment process.

If the Fed cuts rates aggressively in response, fear may spread further, and the downward spiral could continue. The earlier policy mistake of holding rates steady for too long would then become apparent. Only then would the Fed likely start discussing new tools to widen the elasticity of money and stabilize markets again. QE may return. Yield-curve control may also be discussed again.

That might sound grim at first. But investors should not automatically conclude that it is time to leave the market. These processes take time. No one knows whether the tipping point arrives this year, next year, or much later. My current view remains that the bubble continues to expand and that staying invested still makes sense for now.

Not only that, but I also think that, surprisingly, the dollar may strengthen further and that US markets will continue outperforming much of the rest of the world, especially Europe.

Europe’s Inflation Fight And A Looming Contraction

Europe is considerably more exposed to the closure of the Strait of Hormuz than the United States, as it remains heavily dependent on imported energy. But unlike the US, Europe also lacks the financial and structural flexibility to absorb such a shock as easily. The ECB appears far more committed to fighting inflation aggressively, even as economic growth continues to weaken. That creates the risk that Europe drifts deeper into stagflation, with tighter monetary policy increasingly choking off already fragile economic activity.

The structural problems behind that vulnerability are not new. Europe still lacks truly integrated capital markets and continues to suffer from high taxes, regulatory fragmentation, and heavy bureaucratic burdens that increase costs for businesses and slow investment. While the US increasingly relies on deep financial markets, rising asset prices, and credit expansion to sustain economic activity, Europe has a much weaker transmission mechanism in that regard. It is less able to inflate through economic weakness because its economy remains structurally less financialized and less dynamic.

That problem becomes particularly dangerous during external shocks like the current energy crisis. Rising inflation can, in theory, be mitigated by increases in production and investment. However, Europe’s regulatory environment continues to suppress exactly that adjustment process. Domestic production remains constrained while energy costs continue to rise, leaving the economy vulnerable to a prolonged period of stagnation amid persistent inflationary pressure.

At the same time, European policymakers still appear more focused on redistribution and regulation than on structural reform. The answer to weakening growth and falling competitiveness continues to be higher spending, more intervention, and, eventually, rising taxation to stabilize government finances. Large infrastructure and defense-spending plans may provide short-term support, but they are unlikely to solve the underlying structural problems. Instead, they may push interest rates higher while productive private-sector investment remains weak.

The political structure of the European Union itself increasingly adds to the problem. Bloomberg recently reported growing frustration among member states with Ursula von der Leyen's highly centralized leadership style. More and more policy initiatives are coordinated through the European Commission, while the list of political priorities continues to expand. The result is that policymaking increasingly becomes reactive and bureaucratic, slowing the implementation of the focused structural reforms that Europe urgently needs.

Only a major overhaul of Europe’s tax and regulatory framework could meaningfully revive growth and improve its ability to withstand external shocks. So far, however, there is little indication that European policymakers are willing to move in that direction. As a result, Europe risks entering a prolonged period of economic stagnation precisely while the US continues to sustain growth through financialization, credit expansion, and more flexible policy responses. With an ECB tightening into this environment, it might ultimately turn stagflation into outright contraction.

Nevertheless, and regardless of the ECB’s policy path, I continue to think that European markets remain structurally unattractive relative to the United States.

Market Assessment

My market outlook for stocks and bonds remains unchanged. I still think the current environment favors buying dips in equities, while bonds will likely not serve as the hedge many investors still expect.

I’m also not fully convinced by Goldman Sachs’s assessment of the oil market and continue to think that there remains upside potential for oil prices. Even then, I still view oil as a more attractive hedge than bonds in the current environment. Only a meaningful peace deal or a significant de-escalation in the Middle East would materially change that view.

Gold remains relatively weak for now. Over the longer term, however, I remain constructive on gold. Bitcoin has managed to stay above $80,000 so far, currently validating its recent bullish trend. If financial conditions continue to loosen, it may show upside potential similar to that of equities.

On currency markets, EUR/USD has so far remained in the 1.17-1.18 range. However, considering the dynamics discussed above, I continue to think that demand for dollars will likely increase over time, creating renewed upward pressure on the dollar. Technically, a sustained break below 1.17 would need to be monitored closely.

Conclusion

Despite the increasingly bearish takes on financial markets lately, I continue to think that market participants are reading the signs wrong. Inflation is on the rise, but it will likely mark the beginning of a late-stage inflationary boom rather than the beginning of a recession. Of course, the data could change, but so far, the signs continue to point to ongoing US economic acceleration rather than meaningful economic deterioration.

With the current rise in inflation, financial conditions may continue loosening as long as the Federal Reserve avoids meaningfully tightening monetary policy. Inflation itself increasingly helps sustain the boom by supporting asset prices, lowering the real debt burden, and encouraging capital investment and borrowing to be pulled forward. As long as that mechanism continues to function, Trump may ultimately be satisfied with keeping rates steady, while Warsh may be able to justify that stance using measures like the trimmed-mean CPI. If markets continue to price in aggressive rate hikes later this year, they may ultimately be disappointed.

The danger, and something investors should closely monitor, is that this process gradually increases the underlying distortions within the economy. Yet these dynamics can continue for much longer than many expect, especially in today’s highly financialized economic system. The longer inflation remains elevated while monetary policy stays behind the curve, the greater the pressure on the Fed to respond more aggressively will eventually become.

For now, however, the environment suggests that markets will continue “Breaking The Mirror.”

I’m letting go of my failures, erasing the anger,

The demons behind my eyes.

I’m letting go of the past now, done fighting my way out.

I’m breaking the mirror now.Fit For A King - Breaking The Mirror

Have a great weekend!

Fabian Wintersberger

Thank you for taking the time to read! If you enjoy my writing, you can subscribe to receive each post directly in your inbox. Additionally, I would greatly appreciate it if you could share it on social media or give the post a thumbs-up!

All my posts and opinions are purely personal and do not represent the views of any individuals, institutions, or organizations I may be or have been affiliated with, whether professionally or personally. THEY DO NOT CONSTITUTE INVESTMENT ADVICE, and my perspective may change over time in response to evolving facts. IT IS STRONGLY RECOMMENDED TO SEEK INDEPENDENT ADVICE AND CONDUCT YOUR OWN RESEARCH BEFORE MAKING INVESTMENT DECISIONS.

I think you're spot on Fabian. is it a crack-up boom? not sure, but higher is definitely possible, although I imagine a few hiccups on the way. dollar is still the cleanest dirty shirt and I have seen no indication that UvDL is set to relax her grip on her policies, so bad for Europe overall. commodities remain the best place to be in my view, and when the Iran situation does end, and it will, that means metals will soar in my view as energy prices tumble