Blink 182 - The Rock Show

John Maynard Keynes once said, When the facts change, I change my mind. What do you do? Within financial markets, statements from politicians or central bankers can lead to extreme price movements, especially in times of high economic uncertainty.

Whether it is the pandemic, the war in Ukraine, or rising energy costs, it seems the 2020s are a crisis doom loop. If one wants to know how uncertain, a brief look at bond volatility helps, and it is at its highest level since the Great Financial Crisis in 2008.

Economic data from the US this weeks show that there is still nothing that could lead to an end of the Fed’s aggressive monetary tightening. Consumer confidence was comparable to 2005 - 2007, new home sales exceeded analysts’ expectations, and manufacturing prospects were still far away from a crisis. Only housing prices showed the consequences of monetary policy. Housing prices fell for the first time since 2012 compared to the previous month. Jerome Powell was very clear that it would need a slowdown of the economy if one wanted to get inflation under control. Thus, I do not expect the Fed to become dovish at the next FOMC meeting.

In an Interview with the Austrian newspaper Der Standard, ECB chief economist Philip Lane confirmed that the ECB also plans to raise rates substantially at the next meetings of the ECB’s governing council. Additionally, Lane argued that labor unions should hold back at the coming wage negotiations to avoid second-round effects because inflation might stay elevated otherwise.

It is interesting because, after 2008, I cannot remember a year when labor unions were told not to hold back. So, while back then, the argument was that inflation was too low and wage increases would dampen business margins, now it is second-round effects.

The thing is that labor unions negotiate wages where it is about making up for past inflation, so workers want to get a raise to afford the same amount of goods and services before the price increases. It is correct that this would raise costs for businesses that already suffer from high energy prices, but in the end, it would solely mean that the costs of inflation caused by the ECB are redistributed from wage earners to companies.

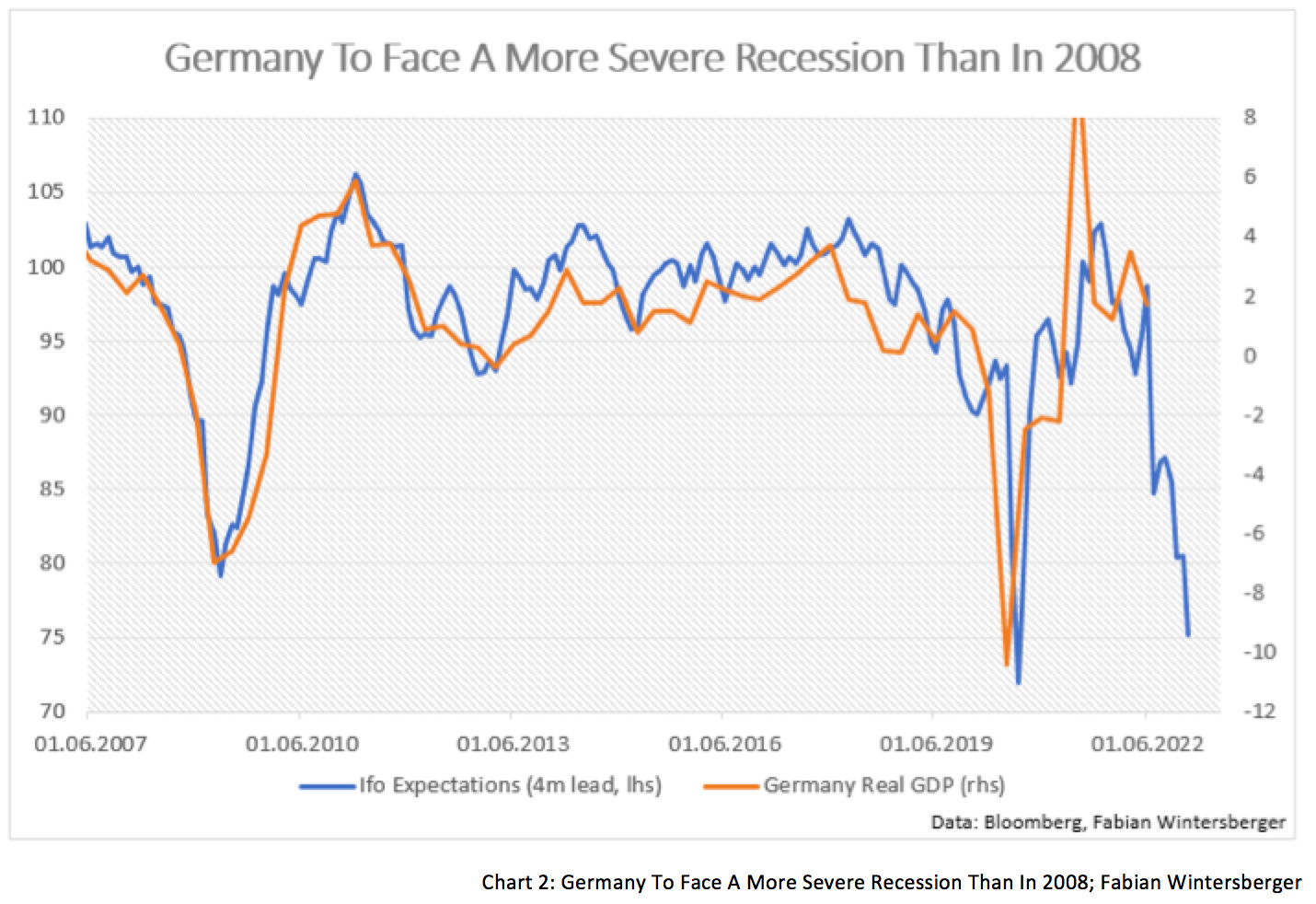

The problem here is that the economic outlook for the Eurozone remains decent due to actual economic and geopolitical issues. Finally, more and more analysts came to this conclusion and cut their growth projections for the Eurozone. This week’s Ifo business climate index suggests that Germany is on the brink of experiencing a recession more severe than in 2008.

However, the difference between 2008 and today is that debt to GDP ratios of European governments have risen substantially since then. Currently, Eurozone debt to GDP is at around 95 %, according to Eurostat, while it was 66 % right before the Great Financial Crisis. Core inflation was close to 2 % in 2007; now, it is at 4.3 %.

Further, European governments have increased their expenditures already during the pandemic to support people and businesses who suffered from the political decisions to fight the pandemic. While during the Great Lockdowns, the affected companies were mainly within the service sector, it is now the industrial sector as well.

The fact that governments follow their policy to fight every crisis with an increase in government expenditures shows that mentally they are still stuck in the age of low inflation. At least one can solve the problems on the surface in times of falling demand, but now the problem is the lack of supply, and one cannot solve this by handing out money to market participants.

Finally, we see the consequences of Keynesian economic policy where solving economic imbalances is procrastinated into the future, leading to more disequilibria. But not only is the Eurozone on its way to a sovereign debt crisis 2.0 but in my opinion, every western nation might be affected sooner or later. This is also true for the US, although it might be the last due to the dollar’s status as the world’s reserve currency.

Now I want to get to the topic that affected markets the most this week. The Bank of England, originally one of the most aggressive central banks in this tightening cycle, became the first central bank that blinked and pivoted.

It was forced to fold after 30y government bond yields nearly doubled in a couple of weeks, from 2.85 %. Markets reacted to Prime minister Liz Truss’s announcement to cut taxes while simultaneously ramping up government expenditures to dampen the effects of skyrocketing energy prices.

The Bank of England raised rates substantially in December last year, ended its bond-buying program, and initially planned to start Quantitative Tightening at the end of September. After rescheduling the previous meeting, it disappointed markets by raising rates only 50 basis points.

Afterward, the exchange rate of the British pound against the dollar fell from 1.12 to 1.04 within three trading days. Besides the decision to hike rates by only 50 basis points, plans from the ministry of finance also played a role, which announced that the tax cut program would cost 45 billion pounds, and it further plans to borrow 400 billion pounds more over the following years.

However, the Bank of England blinked on Wednesday and announced to buy long-term GILTs because the rise in yields led to a material risk to UK financial stability:

To achieve this, the Bank will carry out temporary purchases of long-dated UK government bonds from 28 September. The purpose of these purchases will be to restore orderly market conditions. The purchases will be carried out on whatever scale is necessary to effect this outcome.

Markets reacted, and yields on long-term GILTs posted their biggest drop in a single day in history.

The Financial Times quoted a London-based banker:

‘At some point this morning I was worried this was the beginning of the end,’ said a senior London-based banker, adding that at one point on Wednesday morning there were no buyers of long-dated UK gilts. ‘It was not quite a Lehman moment. But it got close.’

As the Financial Times reported, several pension funds begged the Bank of England to intervene in the market because several were on the brink of collapse as the sell-off in GILTs lowered the value of the bonds they held as assets.

This necessitated funds to sell more gilts to cover their collateral obligations as they hedged future cash flows via interest rate derivatives, so-called receiver swaps.

According to a report (also quoted in the FT article), funds operated with a leverage strategy, partially with a ratio of 1:7(!!). A doom-loop of margin calls and rising bond yields.

On the one hand, the Bank of England calmed down turbulences in the UK government bond market, but as Thomas Sowell correctly notes in his book A Conflict of Visions: Ideological Origins of Political Struggles:

There are no solutions, there are only trade-offs

If the Bank of England buys British government bonds in an environment of rising interest rates to bring rates down, the Bank of England pays money to the bondholder, and the supply of pounds in the market increases. That leads to a fall in the exchange rate, especially against the dollar, given that the Fed continues to hike rates and shrink its balance sheet, which is the opposite of the BoE.

Although it is not the BoE’s intention, its actions lower long-term bond yields, hence the cost of debt for the government. All of that is happening at times when the Truss cabinet plans to spend billions into the real economy to fight a supply crisis.

Meanwhile, the Bank of England could stabilize the pound. Currently, GBP/USD trades at around 1.12. However, we cannot expect the Fed to blink in the coming weeks; hence, it would not surprise me if the pound's exchange rate continues to fall. Chart 3 (note: ends Thursday) shows that the intervention did not lead to a big pound appreciation. Although this changed a bit until Friday, I think that that move will be short-lived.

While QE does not lead to an immediate increase in the quantity of money within the real economy, it does influence prices indirectly because it lowers borrowing costs for governments (and consumers).

I want to remind you of what I wrote last week: In case of a rising inflation regime, a central bank pivot while the government simultaneously ramps up spending, we can conclude that this might lead to a further rise in inflation because demand is propped up while supply falls.

All of the above is true for the UK. On the one hand, the Truss government plans to increase spending to dampen inflation pressures and cut taxes (=lower future income). On the other hand, the BoE has blinked and pivoted and is now loosening monetary conditions via government bond buying.

An expansionary fiscal policy might result in longer-than-expected high inflation instead of a return of inflation to 2 %. That has consequences for asset markets because those prices are indeed influenced by long-term inflation expectations.

Monetary tightening has lowered long-term inflation expectations. Expected inflation in the Eurozone, the UK, and the US have all fallen, expressed in 5y5y inflation swap rates. However, as the BoE announced to intervene, long-term inflation expectations rose substantially on the day and currently are close to 3.8%.

Central bank interest rate hikes will bring down bond prices. However, if inflation stays high, which the market is not expecting at the moment, then long-term bonds are not priced accurately and will move to a more sustainable, lower equilibrium price at some point (=higher yield). To say it with Ernest Hemingway’s words: First gradually, then suddenly.

What does this mean for markets down the road? After the BOE intervened, bonds and stocks rallied, reversed on Thursday, and are now trading a bit higher again.

As always, financial analysts and investors raise their voices and argue that buying long-dated bonds at this level might be attractive. They say that the signs of an economic slowdown are imminent and that central banks will successfully bring inflation down to 2 %. In an environment where central banks have to loosen monetary policy again, they say that bonds with a 4 % yield are an attractive investment.

That is true if inflation falls due to the economic slowdown. However, I have a different view because there are several arguments against it.

The first is that the actions of market participants have changed since the pandemic. Work from home, only minimally spread before 2020, increased massively and is a pre-condition for many to even consider a job offer. In a survey from May 2022, 85 % of UK finance workers say they no longer consider the office as their main workplace.

Thus, demand is shifting from services to durable goods, where production levels are stickier, and therefore it is more likely that prices will rise. If a company wants their workers to work at the office, they might have to accept to pay higher wages than those who offer work from home. That might also contribute to consumer price inflation.

Secondly, there is geopolitical risk. One could expect that China will not be the world's factory and that the production of western consumption goods will probably fall. India, an alternative place of production, seems to align with Russia and China (take this with a grain of salt, I am not an expert in geopolitics). Production will probably have to re-shore in places where unit labor costs are substantially higher. High energy prices are an argument that production will not re-shore in Europe. They are a burden for many European companies already considering moving production to the United States.

Finally, this could mean potential problems for the country with the world’s reserve currency at some point. For years, the US exported inflation (dollars) in exchange for cheap consumer goods, and sellers then invested in the US financial industry and propped up prices there. However, if production is coming back to the US, capital flows back into the country and thus raises the quantity of money in the real economy (=inflation).

As a result, the Fed might be forced to continue hiking rates further than expected, which would prop up the dollar, and foreign borrowers might come under more pressure. But US companies are heavily indebted as well, and at some points, many of them might be unable to service the debt.

If the doom loop that led to the BoE’s intervention occurs in the US, the stakes are much higher. Maybe this will force the Fed to blink and pivot and buy the rising issuance of government debt, or it will have to obligate investors to purchase those bonds with yields below the inflation rate, just as it happened after World War II.

If the Fed monetizes the debt, we might see one last crack-up boom in equities (in dollar terms). If the government obligates investors to buy it, we might see a crash of 1929 proportions. Remember, if an investor is forced to buy a bond, she has to sell something. Therefore, I think that, for long-term investors, bonds and stocks are risky investments because of a very uncertain outcome. Buying bonds at this point more seems like picking up cherries in front of a steam roller.

I think tangible assets would be a better option in that case: commodities, real estate (danger: judgment creditor's mortgage), gold and silver, or (if you are a believer) Bitcoin. Gold and Bitcoin are down big since the tightening cycle started, which led to some investors nagging proponents of those assets, saying that they are no inflation hedge.

However, those people forget that gold is falling because market participants expect that the Fed will succeed in its inflation fight (in EUR and GBP terms, gold is still near ATHs). If central banks do not succeed and/or have to loosen monetary conditions because of market turmoil, then gold (and bitcoin?) will have its make-or-break moment.

And as the events around the BoE, this week showed, this moment can arrive sooner than one might think. So, dear Bank of England, you finally fell in love with the QE at the rock show again.

I wish you a splendid weekend!

Fabian Wintersberger

Thank you for reading! You can subscribe and get every post directly into your inbox if you like what I write. Also, it would be fantastic if you shared it on social media or liked the post!

(All posts are my personal opinion only and do not represent those of people, institutions, or organizations that the owner may or may not be associated with in a professional or personal capacity.)