Biggest & The Best

Acceleration Without A Pivot

The truth is rarely pure and never simple – Oscar Wilde

As the Trump administration is wrestling with domestic political turbulence following the release of the Epstein Files, the geopolitical front remained rather calm this week. In financial markets, the week did not provide any new impulses that would lead to a significant change in expectations.

While in the US, new data releases on the current state of the jobs market gained some attention, European data offered some hope that economic stagnation might finally come to an end. At least, that’s what the headline numbers suggested. As always, however, the situation beneath the surface remains unclear — and that likely explains last week’s decision by the ECB.

ECB To Hold Rates Steady - No Change In Rhetoric

The February meeting of the European Central Bank delivered exactly what markets expected: no change in rates and no change in tone.

Christine Lagarde reiterated that policy remains appropriate, inflation is moving toward the 2% target, and decisions will continue to be taken meeting by meeting, based strictly on incoming data. The Governing Council sees risks as “balanced,” with some factors pushing upward, others downward — but nothing warranting action at this stage.

The most interesting nuance came during the Q&A. Asked about the exchange rate, Lagarde repeated the familiar line that the ECB does not target the euro — but acknowledged that currency movements matter for inflation and financial conditions. It was a reminder that while the exchange rate is not a policy objective, it remains part of the reaction function. Still, she offered no suggestion that recent FX moves would trigger a response.

There was neither a rhetorical pivot toward easing nor any indication that policy has become overly restrictive. No attempt to prepare markets for cuts. And equally, no renewed hawkish edge. Compared with December, the message remains essentially unchanged.

The bottom line is that the ECB remains in wait-and-assess mode — or, as Lagarde and other Governing Council members like to put it, “data dependent” and “meeting-by-meeting.”

As a result, there is little indication that market expectations for rate cuts are diverging from the ECB’s own thinking. Hence, the market’s expectation of zero rate cuts in 2026 appears warranted.

Germany: New Orders Alone Don’t Make A Recovery

The German defense package is beginning to leave its mark on economic data releases. December factory orders rose by a whopping 13% compared to last year and 7.8% compared to November 2025. Clearly, the rise in defense orders has had a significant impact.

At first glance, it may seem easy to conclude that the optimists regarding Germany’s growth outlook were right. Under the surface, however, there are still reasons for skepticism.

Despite the surge in new orders, German industrial production fell another 1.9% in December. This is yet another manifestation of the longer-term downtrend in German industrial production, which peaked in late 2017. Since then, production has trended lower almost continuously. Interestingly, 2017/18 showed a similar pattern: while new orders continued to rise into the first half of 2018, industrial production weakened. Non-defense sectors showed no recovery — only further declines in activity.

Oliver Rakau of Oxford Economics also pointed out that “turnover fell and remains essentially range-bound since last year.” Therefore, in order to expect a recovery beyond current expectations, one would need to see output and turnover follow the spike in new orders. At the moment, that is not happening.

It is also worth adding that the availability of capital — something government spending often aims to “solve” — was never Germany’s main problem. There is ample unused capital sitting in private savings accounts, ready to be deployed. The real issue lies in unattractive investment prospects, largely due to regulatory burdens and structural cost pressures. As a result, additional government spending is more likely to crowd out private investment than to substantially increase overall investment.

Finally, government spending only began in late 2025. Any meaningful recovery is therefore unlikely to show up in first-quarter data. Given the time it takes for investment to translate into output, it seems reasonable to assume that even the second quarter may disappoint those who are bullish on Germany’s economy.

A Hawkish Warsh? Likely Another “Fell For It Again” Award

Shifting our focus from the eastern to the western side of the Atlantic, my warnings regarding Kevin Warsh appear increasingly justified: anyone taking his past statements as a reliable guide to future Fed policy may be in for another surprise.

The Economist recently reviewed his speeches and found that Warsh’s stance has often shifted depending on the political backdrop. Whenever a Democrat occupied the White House, Warsh tended to adopt a more hawkish tone than when a Republican was president. His change of position on rate cuts may therefore not be driven solely by data.

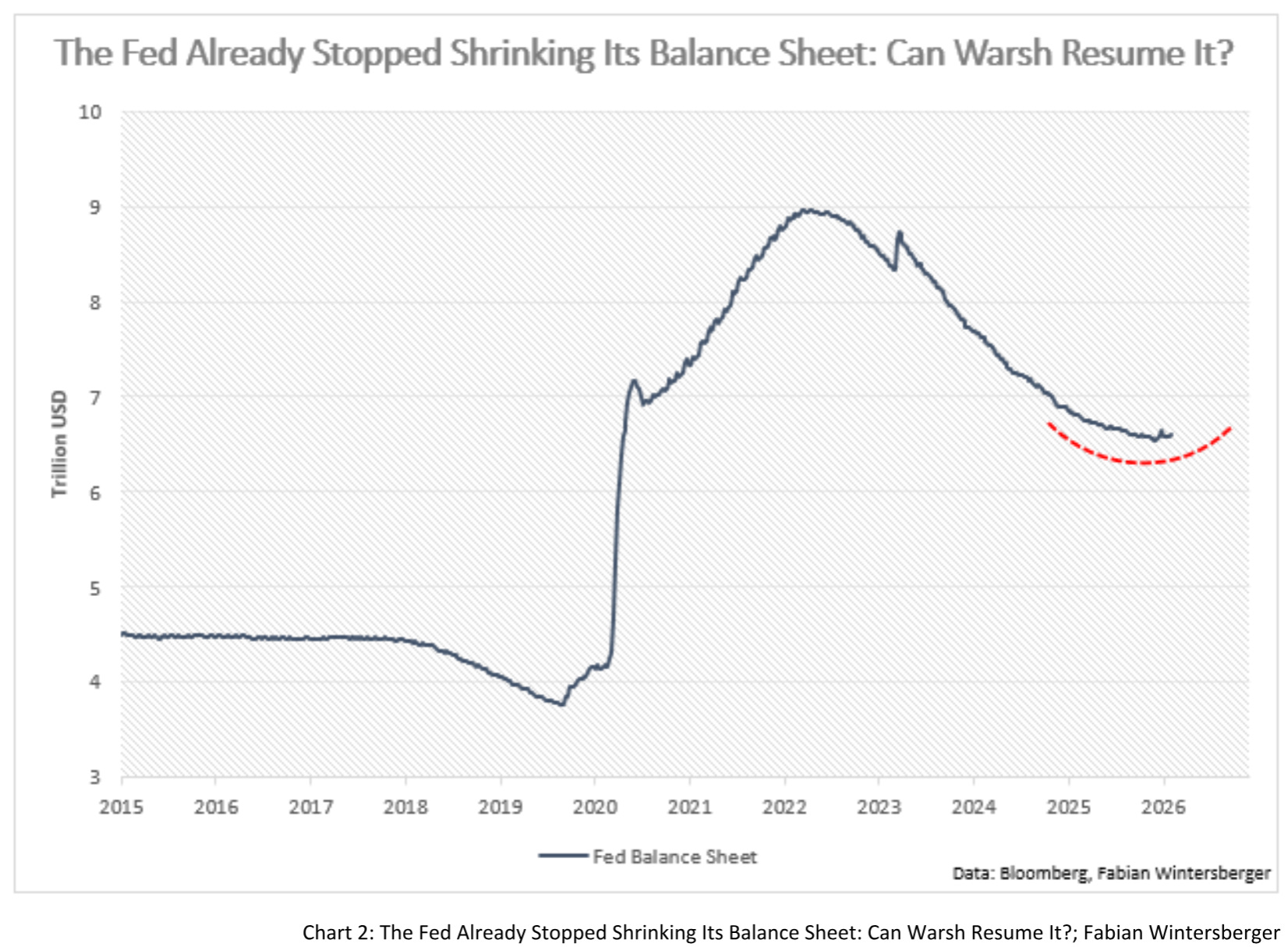

Some argue that Warsh may have changed his stance on interest rates but remains committed to balance-sheet reduction and further quantitative easing. In theory, that position may sound appealing. In practice, the constraints are very real. The more relevant question is whether the Fed would be comfortable with the consequences of a materially shrinking balance sheet. My view is that it would not — and therefore a significant reduction appears unlikely. Even Powell, who frequently emphasizes the need to further reduce the balance sheet, has made little progress over the past six months. The Fed’s balance sheet remains 58% larger than before Covid.

Another factor that challenges the assumption of a Warsh-led aggressive shrinkage is his stated support for closer coordination between the US Treasury and the Fed. Over the longer term, such coordination may point more toward suppressing long-term yields than toward aggressively reducing liquidity — although nothing is set in stone at this stage.

Regarding the balance sheet, Treasury Secretary Bessent noted this week:

I wouldn’t expect them to do anything quickly. They’ve moved to an ample [reserves] regime.. that does require a larger balance sheet. So I would think they’ll probably sit back, take at least a year to decide what... to do.

That does not indicate that rapid balance-sheet reduction is a near-term priority.

NFPs Again Disprove the Weak JOLTs Data

Last Thursday, attention centered on weak US job openings data. Many pessimists were quick to declare that the anticipated economic acceleration was failing to materialize.

Then, on Wednesday, the Nonfarm Payroll report did not confirm that pessimistic narrative. Payrolls increased by 130,000 jobs, above consensus expectations. The report was solid across most components: part-time employment declined while full-time employment rose, multiple jobholders decreased, federal government employment declined, and average hourly earnings increased by 0.4%. The unemployment rate fell from 4.4% to 4.3%, signaling that the economy remains close to full employment.

Yes, last year’s employment data were revised downward by 861,000 jobs, indicating that the labor market was weaker than initially reported. However, given the sharp decline in immigration, upward distortions were widely anticipated. What matters more is the outlook — and this week’s report suggests improvement.

Viewed through this lens, the thesis of accelerating economic activity in the United States remains intact. Weak job openings data do not necessarily signal a cracking labor market but rather a normalization from post-Covid excesses. Moreover, historical comparisons of NFP numbers need to account for structural changes. With lower immigration, the breakeven payroll number is likely materially lower than in prior cycles, meaning 130k may be stronger than it appears in historical comparisons.

Now, let’s assess how this impacts market trajectories.

Bonds & Interest Rates

Despite the recent rebound in long-term government bonds, my overall view on rates remains unchanged. We remain in a sideways trend, with the potential for a gradual price decline, although early signs of a possible reversal are emerging. Nevertheless, I do not believe it is time to turn bullish on bonds — rather, caution is warranted when adopting increasingly bearish positions.

German Bunds appear technically stronger than US Treasuries at the moment. A steepening of the belly of the curve in Europe remains plausible, although momentum has weakened recently and could reverse in the coming weeks.

Stocks

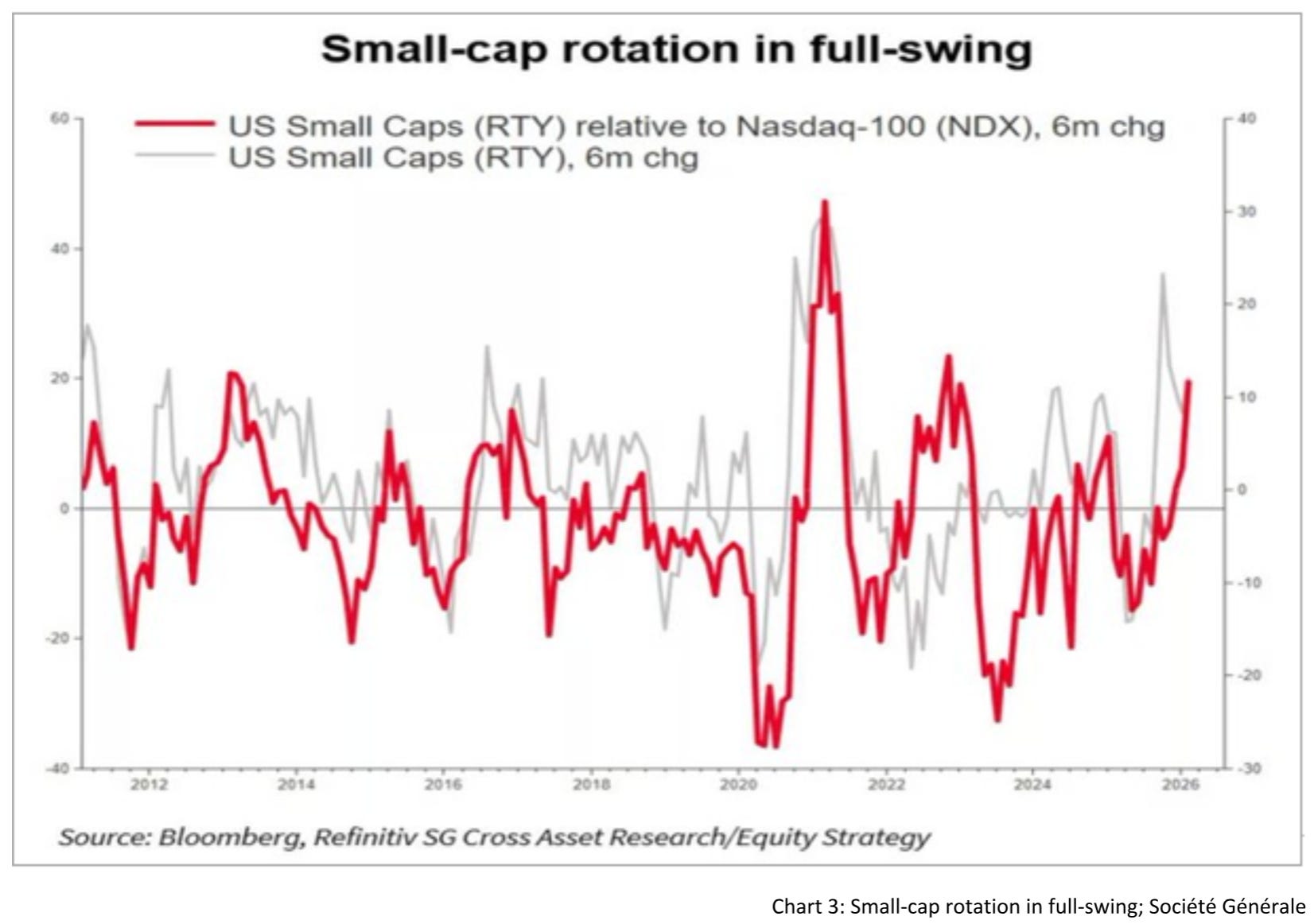

As leading indicators increasingly point toward renewed growth momentum in the US, I continue to view equities as more attractive than bonds. Market breadth appears to be improving, supporting a higher allocation to cyclical stocks such as small caps.

Small caps have already outperformed the Nasdaq 100 over the past six months, as Chart 3 illustrates. If economic acceleration continues, this trend is likely to persist.

FX, Gold & Bitcoin

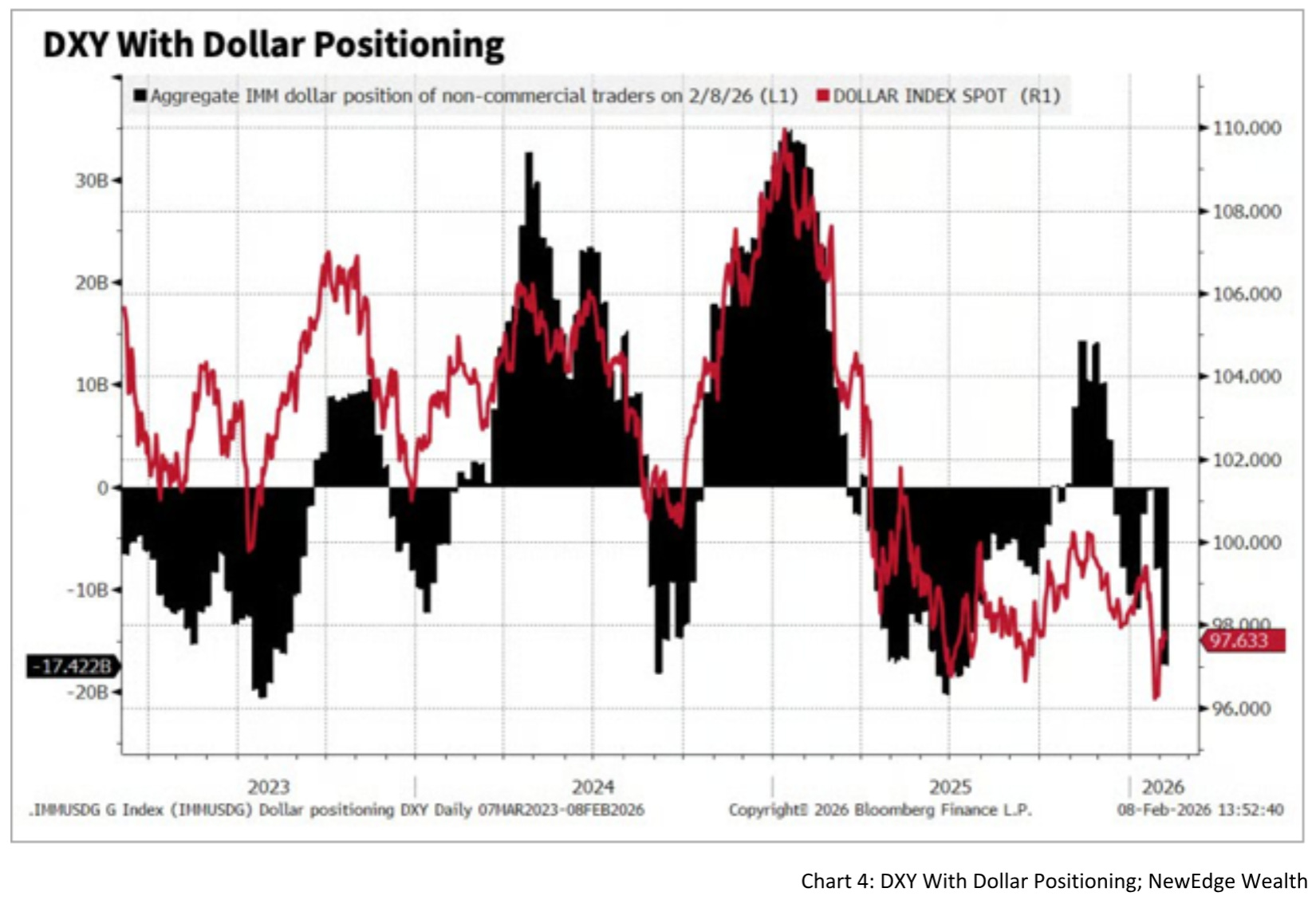

The dollar has weakened further against the euro, keeping EUR/USD in an upward trend. The 1.20–1.25 range remains a potential “danger zone” where reversals could occur. Positioning data show dollar shorts back at 2025 levels, suggesting caution regarding further dollar weakness.

Overall, the broader picture supports my year-end assumption that the dollar may remain in a sideways trend, potentially weakening further in the short term. Over the longer run, however, current weakness may lay the groundwork for renewed strength.

Gold successfully defended the $5,000 level, and the recent pullback appears to be a healthy unwinding of positions within a structural bull market. Bitcoin, by contrast, continues to show signs of weakness, making it difficult to argue that a durable bottom has already formed.

Overall Assessment & Conclusion

Despite the recent recovery in bond prices, the underlying data warrant caution. If the U.S. economy continues to accelerate, US Treasuries—the global anchor for bonds—could quickly lose recent gains.

Equities remain in “flight mode,” supported by global fiscal expansion. While the longer-term consequences of increased state intervention may prove problematic, the short-term effects can be powerful.

For now, it does not appear to be the time to turn bearish.

And if one expects balance sheet reduction to provide meaningful headwinds, the Fed seems unlikely to participate aggressively. The ECB is still engaged in QT, but the point at which it may conclude that process appears to be approaching.

Just as governments compete to deliver higher growth and greater “economic security” through ever-larger spending programs, central bank balance sheets may end up competing over who is the “biggest and the best.” For now, nothing appears willing to stop that train.

I’m the biggest, the best

Better than the rest, better than the restClawfinger – Biggest & The Best

Have a great weekend!

Fabian Wintersberger

Thank you for taking the time to read! If you enjoy my writing, you can subscribe to receive each post directly in your inbox. Additionally, I would greatly appreciate it if you could share it on social media or give the post a thumbs-up!

All my posts and opinions are purely personal and do not represent the views of any individuals, institutions, or organizations I may be or have been affiliated with, whether professionally or personally. THEY DO NOT CONSTITUTE INVESTMENT ADVICE, and my perspective may change over time in response to evolving facts. IT IS STRONGLY RECOMMENDED TO SEEK INDEPENDENT ADVICE AND CONDUCT YOUR OWN RESEARCH BEFORE MAKING INVESTMENT DECISIONS.