Another Hero Lost

War, Markets and the Illusion of Strategic Control

War is the realm of uncertainty; three quarters of the factors on which action in war is based are wrapped in a fog of greater or lesser uncertainty. — Carl von Clausewitz

Finally, what many had speculated about actually happened. Israel and the US launched a war against Iran, reportedly taking out a significant part of Iran’s top political personnel within days. The Ayatollah was killed in the first strike — another demonstration of how precisely Israel can operate.

Looking at the price action prior to the war, bonds appeared to price rising escalation risk ahead of the weekend. The rally into the weekend seemed fueled by financial actors hedging the possibility of escalation — at least the narrative fits.

As is often the case with geopolitical shocks, the initial move turned out to be a fade. Those who thought it was smart to buy fixed income at the Monday open were quickly punished. However, since then, both the war and, as a result, the market have taken unexpected turns.

“Operation Epic Fury” - The Unexpected Backlash

After the first strike, in which Israel/US bombardments eliminated the Ayatollah and a large portion of Iran’s political elite, it initially looked like a decisive win for Trump. Early market reactions and commentary suggested that the US and Israel may have been attempting something akin to a “Venezuela playbook” — only with a killing instead of a kidnapping.

While no one knows for sure, the implied expectation seemed to be that events might unfold similarly: markets would turn nervous, rates would drop, and the Iranian regime could be pressured back to the negotiation table — allowing Trump to extract concessions. Such an outcome would also have implications for the oil market, given China’s significant reliance on Iranian crude.

However, events took a different turn. The “Venezuela playbook” logic stopped working.

After all, Iran isn’t Venezuela. Retaliation followed. Swarms of drones and rockets were launched — not only toward Israel but also toward US bases in other Arab states. The escalation appeared broader than initially anticipated.

Together with shifting justifications for the timing of the attack, it became increasingly clear that markets had largely priced a swift resolution rather than a prolonged confrontation.

In my view, that explains the subsequent market behavior — combined with mispricing that had already built up from a fundamental perspective. As soon as it became evident that escalation risk was not fully contained — while acknowledging Israel’s own strategic motivations — markets turned more cautious.

The bond rally from Friday was sold into as oil opened higher on Monday, before WTI drifted back toward $70. Bonds also stopped declining further, suggesting the possibility that the move was more mean reversion within the prior trend rather than the start of a new regime. The S&P closed green on Monday, while European indices were hit from the start. One plausible interpretation is that markets began pricing relative economic exposure differently — with Europe seen as more vulnerable to prolonged energy instability.

That is what has happened so far.

No one knows how this will proceed. In war, information deteriorates quickly. Traditional media has offered little clarity, while social media is flooded with narratives from both sides — often indistinguishable from propaganda.

What we can do, however, is outline scenarios and think through their market implications. I do not know which path will materialize — or whether markets will react exactly as anticipated. But having a framework provides a compass in periods when uncertainty dominates price action.

Scenario I: From “Epic Fury” To “Epic Victory”

Every war is a matter of logistics and available material. It’s possible that the Iranian side runs out of launch capacity or munitions first. It’s possible that Iranian fighters refuse to continue a war they cannot realistically win. Or, it can be that Trump is offered the “Venezuelan Solution,” where the rest of the regime remains in power, but makes sincere concessions to the Trump administration.

While it’s unclear whether Netanyahu and the Israeli government would agree on such terms, the sheer distribution of power, at least on paper, is in the hands of the US. Another, rather more unlikely, possibility could be that there’s a revolt and a pro-Western government takes over Iran.

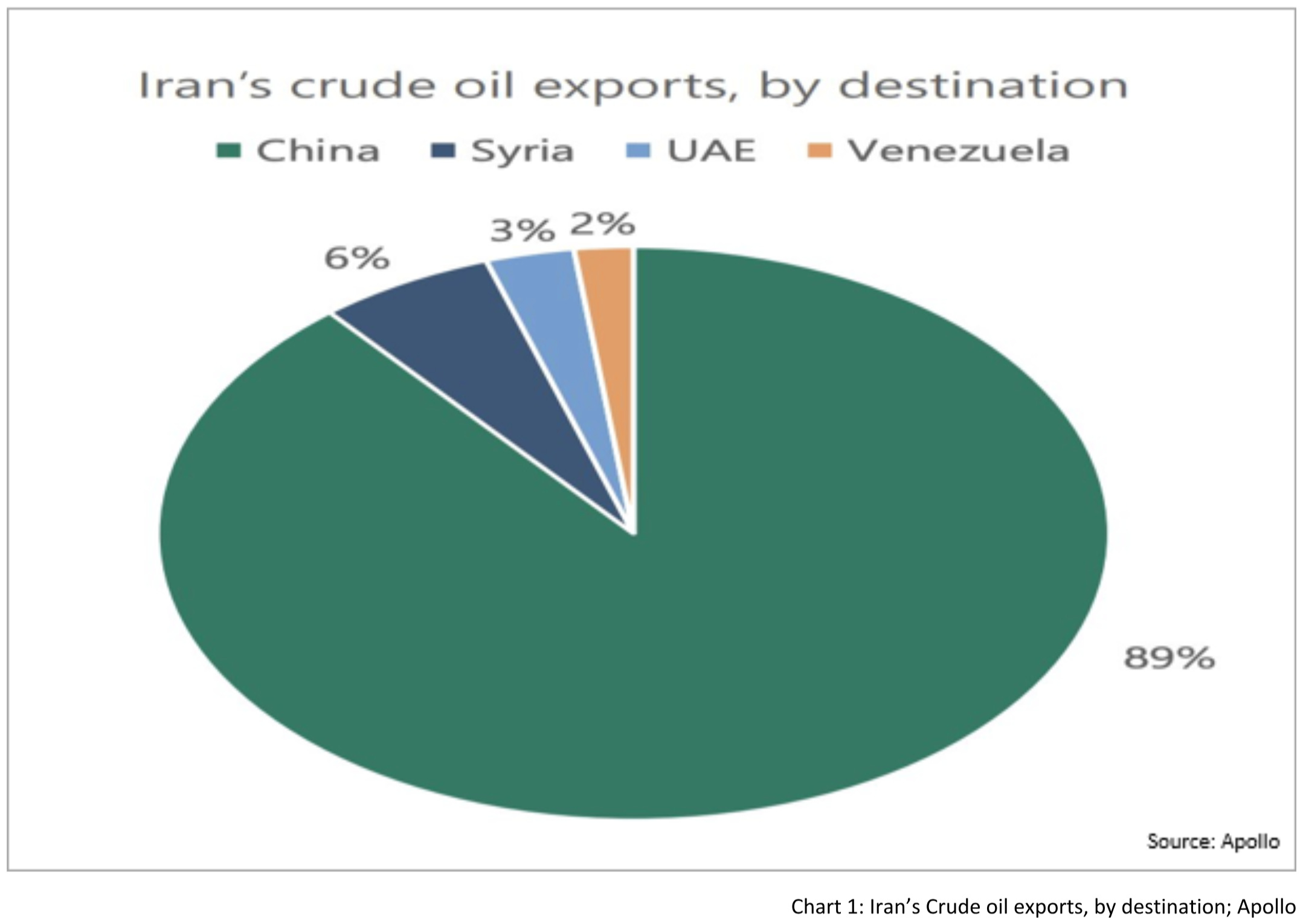

However, for the sake of the scenario, let’s assume the war results in a short one with a decisive win of the US/Israeli coalition where Trump also gets his hand on large portions of Iranian oil that is now shipped to the US instead of China, where currently 80% of crude exports go, according to Apollo.

Because of that, it’s widely argued that China doesn’t have a vital interest in a longer ongoing conflict either. In case of a US/Israeli success, oil supply from Iran would be heavily diminished. If this oil gets redirected from China to the US, then the US benefits from increasing supply that could be beneficial for the economy. It would lower energy prices, dampen price pressures and make production in the US more favorable compared to other parts of the world.

On the second layer, the geopolitical sphere could shift. It could create a balance of power between rare earths and oil, meaning that China controls rare earths (at least so far as they’re not dug up by Western countries) while the US controls the biggest share of the oil market. It would be a balance of geopolitical power that underscores the switch to a multipolar world with the US still being able to shift the balance to its favor if it wants.

It would be a major blow to attempts to build partial trade settlement systems outside the dollar. Those whose aim it was to create a parallel trade architecture would be weakened by the conflict.

In case of regime change or a fragmented Iran, Israel would become the undisputed hegemon in the Middle East. Without a powerful Iran and with the majority of Arab states financially incentivized through US security arrangements, no actor would be able to operate without Israel’s approval. The Palestinians would lose regional support, which would give Israel more leverage in determining their future. It would be the best-case scenario for both Israel and the United States.

In the scenario where Trump is satisfied with the Mullah regime remaining in power, Israel’s position would be weaker, although the substantial weakening of Iran would still be strategically beneficial.

However, what would that mean for markets?

It would likely be a relief for risk assets and could normalize oil supply expectations. Possibly, European stocks would benefit to some degree because they were hit heavily by the possibility of disrupted oil and gas flows from the Middle East, particularly after having abandoned Russia as a supplier.

Depending on how quickly such a victory is achieved — or perceived as achievable — a return to all-time highs in equities would become increasingly plausible. For bonds, the picture is more nuanced, but if lower energy prices dampen inflation while supporting growth, it could allow the interrupted bond rally to resume. Yet, it could also mean higher growth and thus, rising term premia for longer-term bonds while the Fed cuts rates on the front end. The recent yield curve flattening could then become a steepening again.

This scenario, though, is based on the assumption that the Iranians will give up early and that the US and Israel can work something out with them that would guarantee at least immunity for former regime proponents or soldiers of the Iranian Revolutionary Guard. And Iran has already stated that it prepares for a longer war and that it isn’t interested in negotiations.

Consequently, we have to consider a second scenario for the trajectory of the war, which is a prolonged one.

Scenario II: From “Epic Fury” To “Epic Disaster”

As the Trump administration has failed to communicate a clear objective for the war — and as it appears unprepared for the scale of Iran’s retaliatory attacks — the fighting continues. The goal of a rapid collapse of the regime failed spectacularly, as the administration severely underestimated the conviction of the Iranians to fight back.

And so the fighting continues, with the US and Israel intensifying their bombings, while the Iranians hit more and more targets across the Middle East as stocks of interceptor missiles begin to run low, and not every rocket can be shot down. The US and Israel fail to achieve their desired quick victory.

What are the results for the global economy and markets in that case?

As the summer approaches, the fighting is still ongoing, and the Strait of Hormuz remains largely empty, as ships hardly dare to risk going through the passage. The navy was reportedly uneasy about Trump’s announcement that the US would insure ships passing through the strait, and it has now suffered losses while attempting to secure the shipping lanes, achieving next to nothing as attacks continue.

What was initially expected to be a mission of weeks has turned into a month-long operation, increasingly resembling a major human tragedy.

Markets had not priced this scenario. A few days into the war, they were expecting a swift end to the conflict, and the drawdown in bonds seemed to be over, pointing to a potential bottom. US stocks, which were not hit as severely as European or Asian markets, quickly recovered. Oil (WTI) shot up but failed at the $80 mark. At the same time, the dollar also stopped rising further while gold fell back toward $5,100.

But the longer the war went on, the more nervous the market became. US deficits rose as more and more weapons and military equipment had to be replaced. The closed Strait of Hormuz pushed oil prices above $90 per barrel. Long-term bonds continued to drop as markets began pricing another inflationary wave. One-year US inflation swaps rose another 50bps.

A lot of stocks, however, didn’t seem to care much. Higher US government spending and war production increased US GDP and kept unemployment low. In late March, equities returned to all-time highs, as investors looked for places to flee currency devaluation. Gold and Bitcoin also benefited from the developments and the broader rise in inflation expectations.

While war is bad for those who are affected by it, it can be profitable for businesses engaged in it. The military-industrial complex posted one earnings beat after another. The US boomed, and Europe also gained some footing as governments intervened in markets and spent billions more than anticipated to boost military production and buffer the economy.

That also boosts commodity prices, whose acquisition becomes critical in war. In case of a prolonged war and a rising price of oil, mining becomes more capital-intensive and costly, while demand increases because of the war effort.

That increases the demand for dollars, but the Federal Reserve under Kevin Warsh decided that it’s not the time to think about inflation and is in close contact with the US Treasury to dampen the effect of the war effort on the budget. Despite all warnings from economists, the Fed has already cut interest rates twice and signaled that further cuts may follow. Again, markets were totally unprepared for that, and the long end reacts exactly the same as in 2024, when Jerome Powell cut interest rates in a healthy economic environment. The yield curve steepens sharply.

Yet the broader public benefits little from such an environment. Consumer confidence weakens as resources shift toward the war effort, while domestic political pressure to end the conflict gradually increases.

Some of you might argue that the stock market would suffer from a prolonged war. That could be true, and will undoubtedly be true for some parts of the economy and the market, but my thesis is that the broader market — fueled by ETF buying — may continue pushing indices higher. Of course, all this creates a lot of malinvestments and disequilibria — but as long as the economy is directed in that direction and resources are not yet exhausted, these disequilibria will not discharge.

Is It a Geopolitical Genius Move to Cut China Off From Oil?

Of course, both scenarios outlined above remain speculative. First of all, this isn’t a military analysis. Second, wars rarely unfold according to clean analytical paths, and reality often ends up somewhere in between.

Still, thinking through such possibilities provides a useful compass for navigating markets in times of uncertainty — apart from the well-known “nothing ever happens” scenario that markets so often gravitate toward. That, too, remains a possibility.

Yet, I want to discuss another theory that rarely appears in traditional financial media, but receives considerable attention from macro analysts such as Michael Every of Rabobank, as well as from other geopolitical strategists.

The argument runs roughly as follows: the military actions of the Trump administration follow the objective of regaining influence over the global oil market. Venezuela and Iran were allies of China and supplied it with significant amounts of oil. By acting against both, the Trump administration may have effectively restricted China’s access to important strategic oil supply, thereby creating a counterweight to China’s dominance in the rare earths market — a sector that is also critical for modern warfare and the emerging information economy driven by AI.

Seen through that lens, the actions of the administration receive a kind of genius, “5D-chess” interpretation. The theory has circulated widely among macro analysts since it was first popularized by strategists such as Michael Every of Rabobank and later echoed across the macro commentary ecosystem.

However, that still poses the question of how substantial the thesis really is. The theory appears to oversimplify several aspects in order to produce a compelling strategic narrative.

First, the whole argument about the balance of rare earth dominance of China relies on the fact that the definition of “rare” is flawed. They’re rare because the mining is mostly forbidden out of environmental considerations, not because of a lack of accessibility. It’s a result of NIMBY (Not In My Back Yard) policies, not because of geological realities.

Secondly, the oil market is not fixed. The loss of one supplier can be substituted by buying from another supplier. China isn’t isolated there, though resourcing would come with short-term difficulties.

Russia is currently moving away from Europe because of Europe’s aggressive policies toward it and moving closer toward China. Not because of an ideological alignment, but out of necessity.

For markets, the implication is that geopolitical shocks in the oil market rarely translate into permanent supply shortages. They translate into price volatility. If supply from one region disappears, it tends to be replaced elsewhere — albeit often at a higher price and with different geopolitical alignments.

For markets, the more realistic outcome is therefore not a structural cut-off of Chinese energy supply, but rather a period of higher and more volatile oil prices as trade flows adjust.

It could be that Trump and his advisors are proponents of the theory and follow the strategy.

I’m not disputing that.

However, the point is that the administration moves in a way that makes it obvious, in my opinion, that it totally neglects the second and third-order effects of their actions. The theory loses a lot of validity if one strips out the assumption that government bureaucrats are almighty geniuses who can perfectly steer markets and economic developments.

That assumption is questionable for any administration, and particularly doubtful in situations where policy communication itself appears inconsistent.

And so, it’s possible that the theory is based on some merit, but it’s highly questionable that there’s a coherent plan behind it.

Finally, if that geopolitical chess was the plan, the administration would benefit more from explaining it publicly and making a case for it ahead of the mid-terms. The argument that such a strategy cannot be disclosed because it would reveal too much to China is weak — if this were truly the strategy, Beijing would almost certainly already be aware of it.

Currently, there’s no real argument to make why that war was necessary and why it was started from a US perspective.

The Every-argument at least would be an argument that might resonate with some voters who are currently vastly opposing this war and putting American lives at risk for this.

Now, let’s assess the further trajectory for markets.

Bonds & Interest Rates

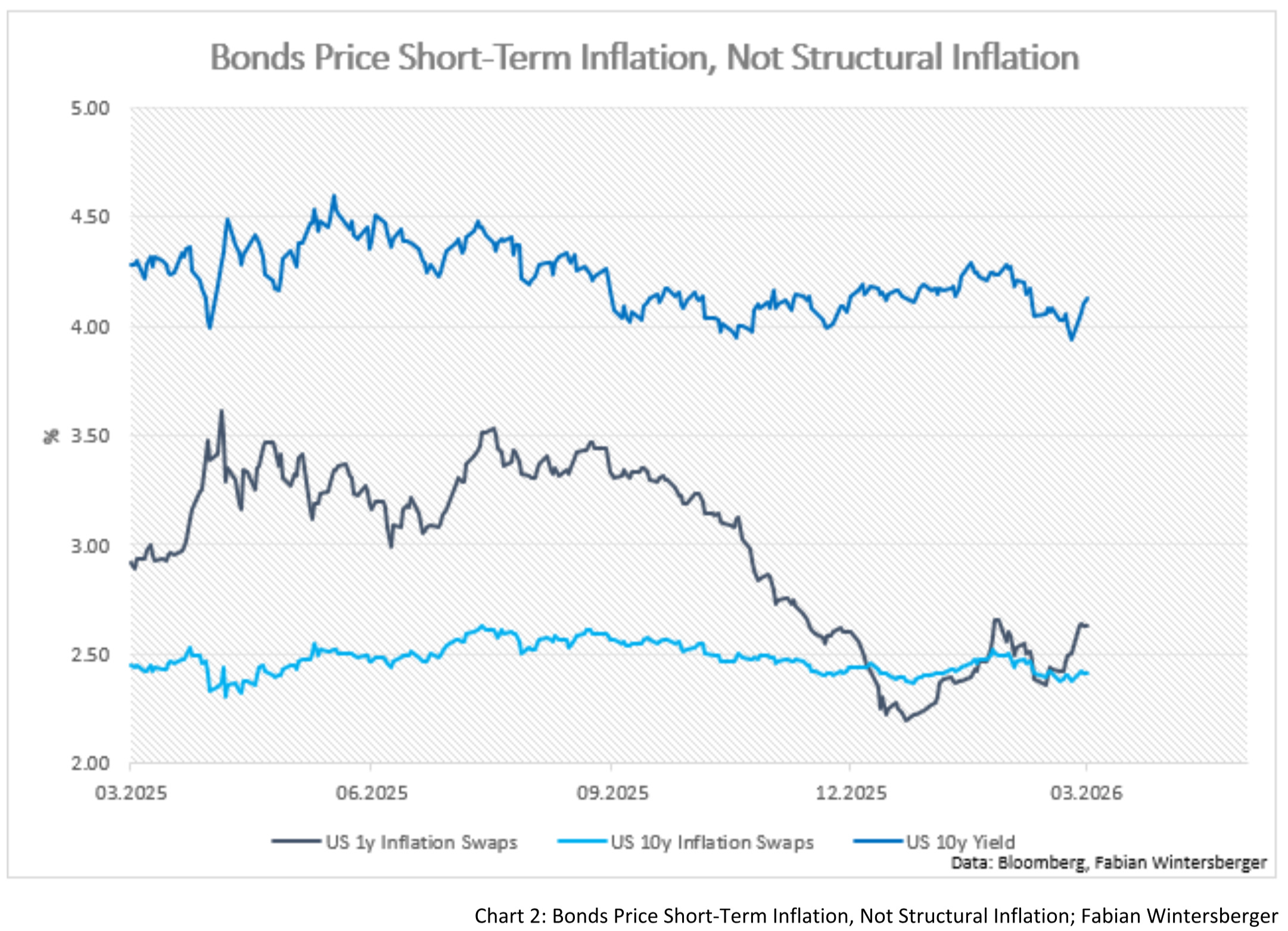

While bonds were bid prior to the war, the start of it turned the page. One could assume that the rise last Friday was a pure hedging move that unwound when the war started, as the market focused on other consequences of the war, such as increasing inflation because of the supply disruptions in the oil market.

Contrary to the claims that this will lead to a more structural return to inflation, the market seems to be way more optimistic about that. The rise in bond yields is mainly driven by the increase of short-term inflation expectations as a result of the war. Long-term inflation swaps have remained largely unchanged and don’t seem to think that the war will last long.

Therefore, it’s unclear whether the drawdown in bonds has led to a real change of trend or was just another extreme mean-reversion that will ease if the expectations of a rather quick ending come to fruition. For now, the situation remains unclear, and therefore, my view has become largely neutral on bonds.

Stocks

As mentioned above, European stocks were clobbered after the start of the war and gapped down in three consecutive sessions before they arguably found an at least short-term bottom, only slightly below where they started the year.

US stocks, on the other hand, almost recovered and the price action remains constructive. As the war trajectory remains unclear, it might be useful to have some dry powder in case of another leg lower. But as things stand now and what the market is pricing, stocks still have a higher chance of rising to new all-time highs than experiencing a more intensified sell-off that drives the market much lower. Interestingly, US small caps are still up 5% while the S&P 500 is flat year-to-date.

FX, Gold & Bitcoin

As always, war has led to an unwind of short-dollar positioning, resulting in a strong upward move in the DXY. Similar to stocks, the dollar seems to have found a short-term bottom, another signal that market participants aren’t extremely worried about an intensifying and long conflict. If that’s the case, the market will soon turn back to economic data instead of geopolitics, and drive the dollar lower again. That’s supported by the technical picture that shows 1.16 as a resistance for EUR/USD. However, in case markets mispriced the length of the war, the EUR/USD could be in for another leg lower.

The picture for gold and Bitcoin remains vastly unchanged from before the war. If anything, the war has moved the market more in gold’s favor. Bitcoin, on the other hand could signal a build-up of another push for risk assets, which would fit perfect into a bullish stocks narrative. However, despite the recent counter-trend rally, Bitcoin is still too low to talk about a change of trend.

Conclusion

With the Iran war, the market faces a stage of increasing uncertainty. So far, no one really can say how that conflict proceeds, and therefore, it’s probably correct to assume that volatility will increase. But, as my scenario analyses describe, the outcome remains highly speculative. Therefore, it’s probably better to remain defensive and to favor cash before making decisions.

Politically, the war has sealed the fate of the Trump administration and the Republican Party for the midterms. As the war faces a clear majority opposition and without the ability of the administration to formulate a clear goal, the Democrats’ chances of overtaking both chambers of Congress seem to be better than ever before, as Trump would like to say.

For those who hoped that Trump would fulfill his campaign promise of being the “peace president,” the anti-war coalition that widely supported him may now have to acknowledge that Trump has become “Another Hero Lost,” having drawn the United States into what many of them see as yet another senseless war.

You’re gone but not forgot

Another hero lost

The sorrow builds with every passing

All the lessons that you taught

And all the light you brought

Lives on in the eyes of your sonShadows Fall – Another Hero Lost

Have a great weekend!

Fabian Wintersberger

Thank you for taking the time to read! If you enjoy my writing, you can subscribe to receive each post directly in your inbox. Additionally, I would greatly appreciate it if you could share it on social media or give the post a thumbs-up!

All my posts and opinions are purely personal and do not represent the views of any individuals, institutions, or organizations I may be or have been affiliated with, whether professionally or personally. THEY DO NOT CONSTITUTE INVESTMENT ADVICE, and my perspective may change over time in response to evolving facts. IT IS STRONGLY RECOMMENDED TO SEEK INDEPENDENT ADVICE AND CONDUCT YOUR OWN RESEARCH BEFORE MAKING INVESTMENT DECISIONS.