Amazonia

The most important thing to remember is that inflation is not an act of God, that inflation is not a catastrophe of the elements or a disease that comes like the plague. Inflation is a policy. - Ludwig von Mises

If one has read some statements from politicians or central bankers, one could feel that they do not like to get blamed for inflation. Instead, they are quick to blame it on someone else.

Let us remind what has happened in the past years. When consumer goods and services became more expensive in 2021, they tried to calm the public down. Firstly, everyone said it is just pent-up demand pushing prices.

Simultaneously, the central bankers said, supply chains were distorted because of the plague pandemic, causing a shortage of goods and rising prices. But over the medium or long term, no one should worry. As soon as supply chains are back, inflation will be gone. Or that’s what they said.

Inflation is only transitory, and because of that, every Western central bank resisted ending its loose monetary policy. Throughout 2021, the Bank of England, the ECB, and the Fed continued to buy bonds and pump liquidity into markets.

For example, from March 2020 to March 2022, the Fed’s balance sheet more than doubled, and the ECB’s expanded by nearly 90 %. A big junk of this extra liquidity flew into the real economy as European and US governments ramped up fiscal spending. As a result, the money not only elevated asset prices (as post-08) but also consumer goods.

When central banks recognized their mistake, excess liquidity spreaded through various economic sectors. A Russian invasion of Ukraine did not help to improve the situation, but it was a welcomed scapegoat for the pick-up in inflation.

Yet, the ECB somehow hedged itself when it started to fight inflation, claiming it could stay higher for longer because of the green transition. Furthermore, the ECB recently found another scapegoat for the current inflation: greedy businesses that increased their profit margins.

Yet, what is continuously overlooked is that those reasons are just the valves through which the newly created money makes its way.

A market economy is an organic system, similar to the Amazon in South America. In the same way, as human influence shook up the ecological system in the Amazon, central banks mixed up the ecosystem of the market economy.

Critics have already found out who is to blame for the destruction of both systems: Capitalism or greed for profits, which is inherent within the capitalist system according to them.

However, one should add that the current monetary order is much more similar to the one Karl Marx envisioned in his Communist Manifesto than capitalism in its purest form. Marx called for the centralization of credit in the hands of the state, and more-or-less, central banks are trying precisely the same by setting the interest rate.

Last week, central banks got into the center of market participants' attention again. The ECB and the Fed announced their latest interest rate decisions. Market participants hoped that the latest inflation numbers could help them get a clue about the path of monetary policy in the coming months.

Let me start with the ECB, which announced its interest rate decision last Thursday. As expected, the ECB raised all three key interest rates by 25 basis points. The Deposit Facility Announcement Rate is now 3.5 %, the Marginal Lending Facility Announcement Rate is 4.25 %, and the Main Refinancing Rate is 4 %.

According to the read statement from Madame Lagarde at the press conference, the ECB now expects that eurozone inflation will average 5.4 % in 2023, 3 % in 2024, and 2.2 % in 2025. However, the ECB also revised its core inflation outlook upwards due to the latest upward surprises of core inflation and the continued strong labor market.

Although economic activity has stagnated in recent months, the ECB forecasts that growth will come back later this year. Again, Lagarde said that eurozone governments should cut back on fiscal spending, which was ramped up to dampen the consequences of inflation.

Fiscal policies should be designed to make our economy more productive and gradually bring down high public debt. Policies to enhance the euro area’s supply capacity, especially in the energy sector, can also help reduce price pressures in the medium term.

- Christine Lagarde

However, the situation remains uncertain, Lagarde said. Therefore, the ECB governing decided that future decisions on its monetary policy will be data-dependent. Still, Lagarde assured, bringing inflation back to the ECB’s 2 % target will remain the ECB’s top priority.

During the Q&A, Lagarde said that, most likely, there will be another rate hike at the July meeting. Lagarde declined to make any statement regarding rate hikes at the meetings later this year. In contrast to the Fed, nobody within the ECB is considering pausing.

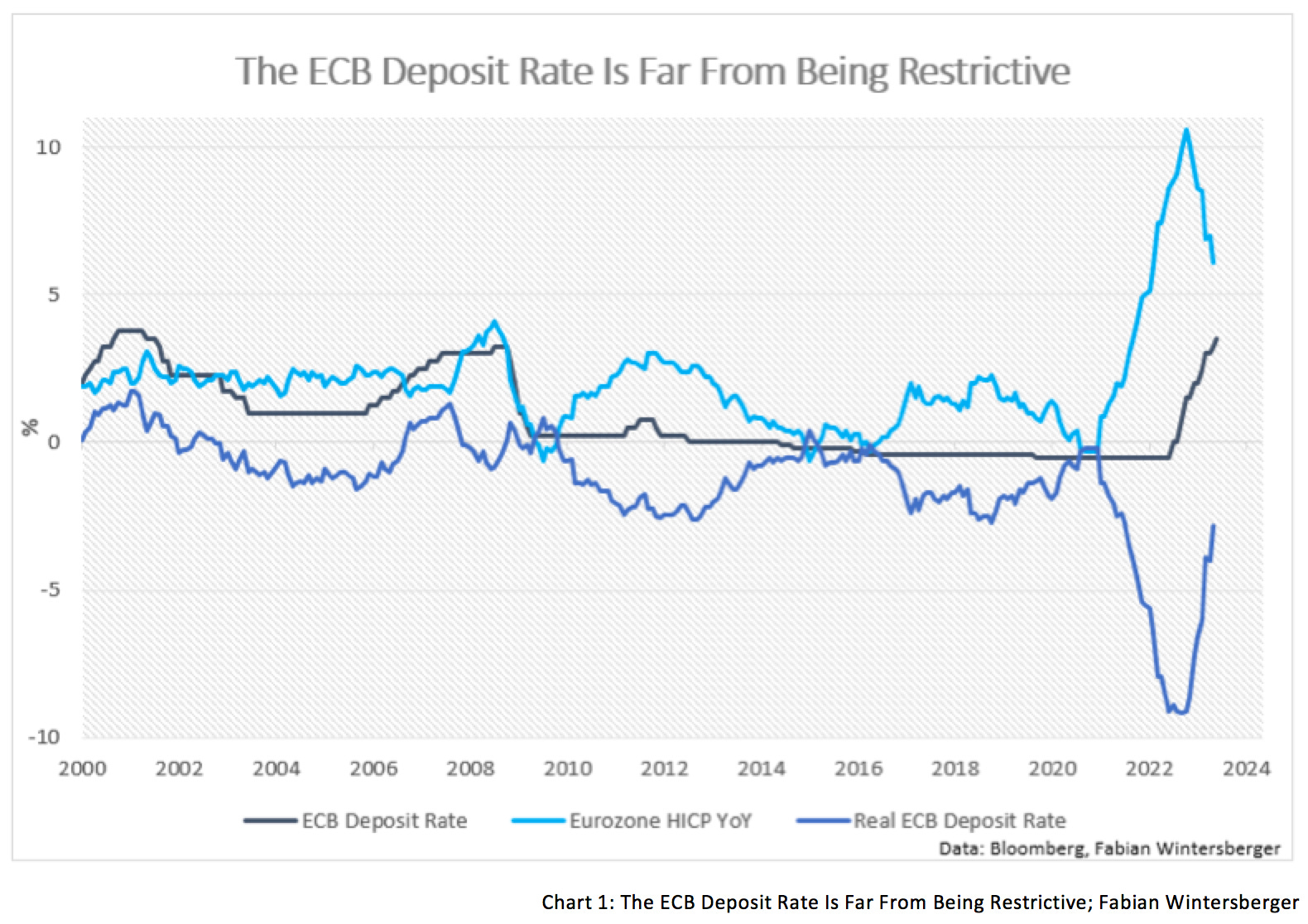

Nevertheless, a closer look at real rates suggests that the ECB’s interest rate policy is still not restrictive enough. If the ECB wants to bring inflation back to 2 %, it should also increase interest rates after the July meeting. A terminal rate of 4 % seems too low; therefore, I still think the terminal rate will end up higher than market participants expect.

Undoubtedly, financial conditions tightened due to the latest rate hikes. An extremely low unemployment rate, core inflation above 5 %, and wage growth above 5 % support the thesis that the terminal rate must be above 4 %. Within 77 % of all 33 goods groups within the consumer price index, inflation is above 3 %, which shows how broad inflationary pressures have become.

On June 19, Isabel Schnabel held a speech at the Euro50 Group called New Challenges for the Economic and Monetary Union in the post-crisis Environment. In the speech, she said that inflation risks in the euro area are tilted to the upside, despite recent weakening price dynamics from a business perspective.

Schnabel made an important point here: the forecasts assume that there will not be another economic shock. Because of that, she pointed out the future path of inflation is highly uncertain. One should remember here that former Credit Suisse economist Zoltan Pozsar made similar remarks on why the increasing uncertainties, especially regarding geopolitics, support the assumption that inflation will settle at a lower level in the coming years.

Additionally, Schnabel said it is a higher risk to do too little than too much when fighting inflation. She listed three points in her speech supporting the thesis that inflation could stay elevated longer.

Firstly, Schnabel talked about the danger of a negative supply shock because of climate change. If such an event leads to a falling food supply, food prices increase, for example. One may add here that current policies in the EU regarding the green transition and resulting sharper rules for agriculture also could contribute to falling food production in the coming years.

Secondly, Schnabel talked about the effects of hysteresis that might affect economic activity. Falling investments and higher demand for labor due to falling total work hours because of increased sick leaves tendentially lead to rising marginal costs for businesses and potentially rising consumer prices.

Thirdly, there is a risk that aggregate demand does not fall as fast as anticipated, which suggests that monetary and fiscal policy is not restrictive enough. All those things make it difficult to quantify the correct level of interest rates.

While some analysts assume that inflation will drop sharply in the coming months due to the latest collapse in producer price inflation, I still think that inflation will remain sticky in the euro area. While headline CPI might fall back into the 3-4 % area quickly in the coming months, core inflation is unlikely to fall below 4 % until year-end.

Now, let us see what happened at last week’s FOMC meeting. After the Fed raised the Federal Funds Rate 10 consecutive times, it paused and kept them at 5 - 5.25 %. This time the Fed wants to see data to assess what the latest rate hikes have done to the US economy.

Yet, according to Powell's opening statement at the press conference, the Federal Open Market Committee thinks it will likely raise interest rates further until year-end. However, it was already visible in the new dot plot, published simultaneously with the FOMC decision. Powell said these steps are necessary because the US economy continues to grow this and next year, as consumption remains strong and the labor market tight.

On the other hand, Powell acknowledged that the housing- and the financial sector already feel the results of the rise in borrowing costs. How the Fed will proceed will be dependent on the incoming data. Again, Powell emphasized that market participants should not expect rate cuts for the next few years.

All in all, Powell’s press conference felt a little strange. As previously mentioned, he said that no one should expect rate cuts for years, and just a few minutes later, he said no one should pay too much attention to the forecasts.

In my opinion, the pause at that meeting does not make much sense. How much incoming data will appear in the coming weeks to see if the latest interest rate increases have been restrictive enough? Further, real interest rates are still at historically low levels.

Despite the Fed pivot in 2022 and the fastest rate hikes since the 1980s, consumer price inflation remained stickier than many would have expected. However, an observation of real rates shows that the Fed Funds Rate is still not restrictive enough, as the real FFR is currently around 1 %.

Suppose one looks at real rates from a US inflation-protected treasury bond perspective, as done by an analyst from Piper Sandler. In that case, the latest rate hiking cycle is far from being exceptional; quite the contrary. During the hiking cycles of 2004 and 1994, the real rate hiking cycles have been steeper than the current. Nominal rates seem to be restrictive, but what counts for economic activity are real interest rates.

The US indices were hardly affected by the FOMC decision. Currently (June 22), the S&P 500 and the Dow Jones Industrial Average have lost about 0.2 %, the Russel 2000 0.6 %, and the Nasdaq Composite, up 32 % year to date, lost about 1 %. Market participants seem uncertain if Powell’s higher-for-longer is indeed true.

Interest rates also did not move much. The short end of the curve is almost unchanged, a bit higher, while the long end fell marginally. It could be that market participants only slightly dissent if the end of this hiking cycle is finally reached or if there will be one or two other rate hikes of 25 basis points.

Danielle DiMartino Booth (fmr. Dallas-Fed) meant that one should not pay too much attention to the dot plot. If one looks at the dot plot at the year-end of 2021, where most FOMC participants expected rates in 2023 at 2 - 3 %, one probably knows why. According to DiMartino Booth, people should focus more on Quantitative Tightening. Can the Fed re-steepen the yield curve via QT? Assuming that the Fed keeps short-term rates at current levels and sells long-term US treasuries back into the market, the additional supply and about 1.5 trillion of new issuances from the US treasury might push long-term yields upwards.

How fast US CPI is going down depends on future price developments. Due to base effects, one can expect another drop to the 3 % area, but afterward, there is a possibility that inflation might accelerate. For a year, core inflation has been rising at a pace of 0.4 % month-over-month. If the trend continues, core inflation will still be at 5 % a year from now. And that is far away from the Fed’s 2 % goal.

As a result, I assume that inflation risks remain in Europe and the US, in my opinion, at least until year-end. Especially core inflation will remain sticky, and a significant drop is still unlikely in both currency areas. From the current point of view, I would not bet that the Fed is done with rate hikes. Also, the expected ECB terminal rate of 4 % is too low, in my view. I see the ECB terminal rate at around 4.5 %.

Rising financing costs due to rising interest rates made bonds an attractive alternative to equities. In the US, the S&P earnings yield, corporate bond yields, and short-term treasury yields are at the same level.

At first sight, one could assume that this is the time to buy bonds and sell stocks. While this might be true from an investor’s perspective if one’s investment horizon is longer than a year. If so, it could be an attractive trade.

Short-term, I do not believe it is. Although the fear-and-greed index shows rising greed, the sentiment among equity traders seems to remain bearish. Regarding bonds, it is the exact opposite. As everyone is anticipating a recession/pivot, most seem convinced that now is the time to buy bonds, but many have said that for at least a year.

I share the opinion of Isabel Schnabel that inflationary dangers are tilted to the upside. Consumption is still strong because of the redistribution from the bottom to the top, the growing investment alternative, and higher interest rate income for the wealthy. Therfore I conclude that the trend will continue for some time. This will keep the economy strong, but the question is, how long.

While my previous hunch was that the recession might start around Q3 or Q4, I think it is more probable to start in Q4. Most analysts expect a mild recession in 2024; from the current standpoint, it looks like a safe call. Therefore, I think the recession will be harsher than expected in Q4. Currently, economic data is still too strong if one neglects the weakness in the manufacturing sector. But as we all know, things happen gradually at first, and then, suddenly.

Financial markets resemble a jungle, and manipulating the ecosystem from central banks has upset the system's equilibrium. It will take until year-end or 2024, until the contracting money supply will unfold its true effect. Then, it will be too late for central banks, and they will overreact another time.

Burn - another gold mine is unveiled

The source of our sorrow

Learn - embedded in this walls of green

Is the curse that we followGojira - Amazonia

I wish you a splendid weekend!

Fabian Wintersberger

Thank you for reading! If you like my writing, you can subscribe and get every post directly into your inbox. Also, sharing it on social media or liking the position would be fantastic!

(All posts are my personal opinion only and do not represent those of people, institutions, or organizations that the owner may or may not be associated with in a professional or personal capacity and are no investment advice. I may change my view the next day if the facts change)

Would it be too much of a conspiracy theory to believe that the Fed, ECB and BOE all encouraged the Russian invasion of Ukraine as a way to divert attention from their own failures and create another scapegoat?

I agree that core inflation will be far stickier than many currently assume, and in fact, may have trouble going below 3.5% for a very long time. Have a good weekend