A New Beginning

It took two years for the Federal Reserve to raise interest rates back up from zero. During the beginning of the coronavirus pandemic, when almost the whole world started to go into lockdown, the FOMC slashed rates by 100bps in an extraordinary meeting. The rate hiking cycle has officially begun.

Some market participants thought that the Fed would even hike by 50bps, but most FOMC-members were clearly against that. Only James Bullard voted for a 50bps rate increase, and the total voting count was 8:1 for a 25bps hike.

At first sight, markets didn’t seem to be too happy about the rate increase either, probably concerning the latest YoY inflation number of 7.9 % and whether that was enough to combat it. The S&P lost about 80 points after the announcement but rallied back during the press conference.

Rates moved in the opposite direction. After the announcement, the US 2y yield jumped to nearly 2 % and pared many of that gains during the press conference.

The US dollar rallied after the announcement, pared its gains afterward, and is now lower than before. EUR/USD currently trades at 1.1073.

One of the reasons behind the rally in stocks during Powell’s press conference could be his optimistic view on the current and future development of the US economy.

Powell spoke very positively about the US labor market and pointed out that the situation has improved substantially, especially for low-income workers, Hispanics, and African Americans. The tight labor market will support future wage increases, Powell said.

According to him, the US economy is still expanding, and the current crisis in eastern Europe will not change that. He dismissed the notion that there is even a slight probability of a recession, and the Fed is still projection real economic growth of 2.8 % this year. However, this is 1.2 percentage points lower than the Feds’ previous projection.

Regarding inflation, Powell said the obvious, namely that it will stay here for longer than the Fed has expected. He pointed out that this is because of robust consumer demand on the one hand and on the other hand because of longer-than-expected problems with the supply chain. The war in Ukraine might also push up inflation in the short term.

Nonetheless, the Fed sticks to its forecast that inflation will gradually move back towards its’ two percent target, just slower than previously projected. When Powell pointed out that the main goal now is price stability and that the Fed will be determined to achieve that, the market rallied on that comment. Future inflation projections YoY are at 4.3 % in 2022, 2.7 % in 2023, and 2.3 % in 2024.

Only the question of when and how fast the Fed will reduce its balance sheet remained unanswered. Powell said that the FOMC would decide on one of its future meetings. Some analysts guess that the balance sheet run-off might start in May.

Obviously, the market has shrugged off its fear of higher interest rates because Powell did not tire of ensuring market participants that the US economy is doing very well. Especially the dismissal of any potential recession risk was cheered by markets.

So, is this the new beginning of a sustainable rate hiking cycle where the Fed achieves to keep the economy in expansion but hinders a potential overheating and tames inflation by gradual rate increases? I will get back to that in just a moment.

What do market participants expect? Currently, they are expecting a very aggressive Fed and six more 25bps rate increases for the rest of the year.

There is a saying that the best cure against high prices is high prices. When the price goes up, demand goes down. At a certain point, households confronted with higher prices have two choices: either to spend their savings or to lower the number of goods and services it buys in the marketplace. However, increased savings of households during the pandemic are long eaten up and only did affect mid- and high-income households.

Thus, it is easy to conclude that continuing high inflation leads to a slowdown of economic activity. US retail sales numbers in February disappointed, and with inflation still at high levels, the trend might continue.

The weak US-Empire State Manufacturing Index also does not support Jay Powells’ thesis of a strong, expansionary US economy. Instead of the expected 6.4 points, the Index was at -11.8, a big disappointment. The lack of optimism among small businesses indicates that businesses are already anticipating a cooling US economy.

I think that the Federal Reserve and its economic departments are well aware of that. Always be cautious about the statement of a Fed member when it comes to future projections of the economy. It is not the Feds’ job to tell the truth. The Fed is always the cheerleader of the economy and wants to spread a good mood. It is all about storytelling, especially in that beauty contest called the stock market.

The bond market has a somewhat more realistic picture of future economic developments than the Federal reserves, especially regarding inflation or economic growth. The bond market supported the transitory narrative for the whole year.

But I think that the main reason is that the bond market is telling that it does not believe the story about a growing, healthy real economy. Especially when the Fed is starting to hike rates into a slowing economy, the economy can go back into recession very quickly. 2s10s 1y forward OIS spreads are already flashing red.

It is not only Overnight Index Swaps that are signaling trouble. It is the same with 5s10s, which turned negative on Wednesday during the FOMC meeting and is now close to zero. And it is the same with the Eurodollar yield curve. The market is not convinced that the Fed is doing the right thing.

While Powell acknowledged that supply chain disruptions would remain in place for longer, China is currently demonstrating that. The country suffers from the worst covid outbreak since the pandemic has begun. The Shenzhen province (17.5 million habitants) has been in total lockdown since last Sunday; factories are closed. In Shanghai, local authorities implemented new restrictions because of a rapid rise in infection numbers. Bad news for the cargo industry, according to freightwaves.com.

According to the article, Chinese ports are all working as usual, and the closed factories even help Chinese harbors stabilize supply chain flows. A closing of Chinese ports would help to relax the crowded situation at US ports, according to George Griffiths (managing editor of global Container Freight at S&P Global Commodity Insights).

However, the article notes that the situation could backfire, and the port situation could worsen again because demand did not go away just because factories or ports closed. Nevertheless, this and other news show that the problem with international supply chains will take a long time until it is resolved and the situation relaxes.

Whether you look at China with the worsening of its covid situation, the easing by the PBoC to support the economy, or the war in eastern Europe and its consequence for commodity markets, I am convinced that in the short term, inflation will remain stubbornly high.

Many might think that in this situation, the Fed would have done better had it raised interest rates by 50bps, which is probably correct, but I think that the Fed is playing time with its 25bps rate hike. It hopes that the economic environment will make the inflation situation go away.

I may repeat, but you cannot fight 8 % inflation with hiking rates by 25bps. The notion that there might be six more 25bps rate increases this year is also not very hawkish, in my opinion. From Washington to London to Frankfurt, central bankers hope that the market will make the inflation problem disappear.

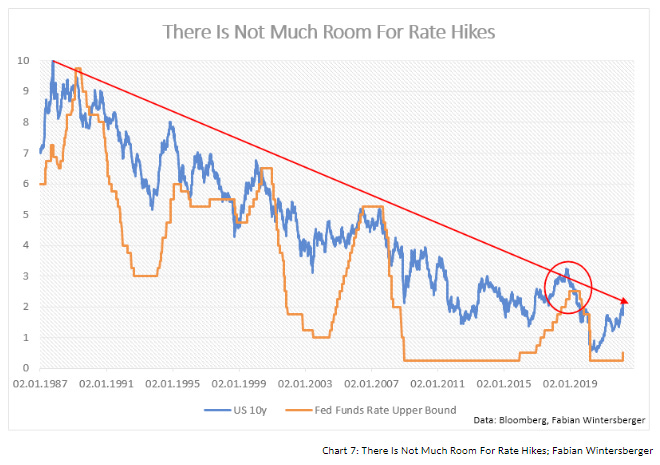

If you study the latest interest rate hiking-cycles from the Fed, it could never raise interest rates back to pre-crisis levels. During the latest hiking cycle, long-term rates already fell sometime before the Fed started to ease again. As this was the US's first interest rate hiking cycle with QE in place, I would argue that the current level of 10y yields (at 2.15%) is probably even too high.

Hence, I think that the Fed is correct that disinflationary forces will take over again. The bond market, Eurodollar, no matter where you look, the market is not convinced that Powell’s intended soft landing will work. Again, I may repeat, but the new hiking cycle might become the shortest in Fed history.

If economic activity is slowing (and there are reasons to assume that it might already), the Lacy Hunt argument about diminishing marginal productivity of debt is becoming dominant again, and deflationary forces are taking over again. One more deflationary shock would be the result.

After that, it will not depend on central banks anymore but fiscal policy. I think that central banks did everything they could in the covid pandemic, and I have to admit that I was wrong to assume that this crisis already turned the tide. I thought that the start of government credit guarantees would mark the end of the deflationary regime because it channeled newly created money into the real economy (and caused inflation).

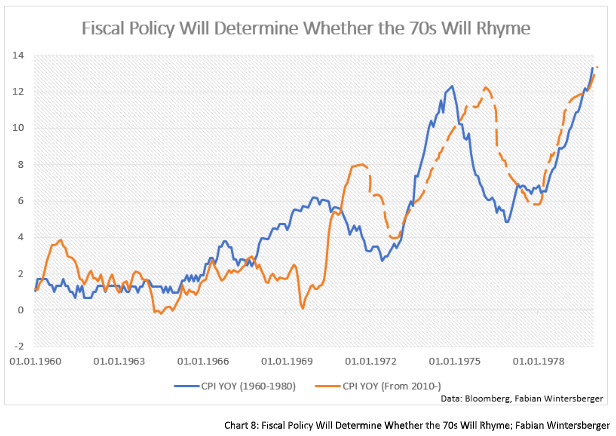

But governments stopped it, surprisingly. However, I think that next time, politicians will not stop it, and Keynesians and MMTers will succeed in convincing them to proceed with those policies. Then, the 2020s may rhyme to the 1970s, when new money flows into the real economy. Regarding inflation rates, the 2010s were surprisingly similar to the 1960s. If fiscal takes over, this trend will continue.

Hence, the latest rate hike may have marked the end of an era and a new beginning, but not a new rate hiking cycle.

Have a great weekend!

Fabian Wintersberger

Thank you for reading! You can subscribe and get every post directly into your inbox if you like what I write. Also, it would be fantastic if you shared it on social media or liked the post!

(All posts are my personal opinion only and do not represent those of people, institutions, or organizations that the owner may or may not be associated with in a professional or personal capacity.)

Thank you for reading! You can subscribe and get every post directly into your inbox if you like what I write. Also, it would be fantastic if you shared it on social media or liked the post!

(All posts are my personal opinion only and do not represent those of people, institutions, or organizations that the owner may or may not be associated with in a professional or personal capacity.)