A Little Piece Of Heaven

Every person in the world probably knows Bohemian Rhapsody by Queen. It is a rock classic, and I assume that many people listen to that song every day.

The way the song is pushing boundaries and how they mix a colorful potpourri to a perfect whole makes the piece a musical masterpiece, in my opinion.

And while you know Queen, it is not so likely that you know the band Avenged Sevenfold. The group from Huntington Beach, California, is a nobody compared to Queen and an insider tip among rock music fans. However, one specific song stands out and is very special, mainly because it is a pretty untypical song for an American Heavy Metal band.

A Little Piece of Heaven. The song is, as Bohemian Rhapsody, a wild mix of various styles of music. With around eight minutes in length, the piece is very long and sounds more like a song from an opera than a rock song. Apart from bass, drums, guitars, and vocals, there are also violins, trombones, and heavy usage of choirs. This wild mix of styles combined makes the song a real work of art.

If the song were published today (and not in 2008), its’ lyrics probably would cause a lot of discussions. All in all, it is a very, very dark lovesong, probably X-rated.

The song is about a couple where the male protagonist is so in love with his girlfriend that, full of fear that somebody might take her away from him, kills her to keep her forever. But unexpectedly, the dead female protagonist returns, plagues him, and takes revenge, and she kills him too.

Now that they both are in hell, he explains his actions to her. Afterward, they decide to prove their endless love for each other. They crash a wedding, kill the bride and groom and then marry at the very same wedding.

For weeks now, I have knuckled my head about one question: Why are interest rates so low? Many tweets recently crossed my timeline, claiming that the real reason for low-interest rates is not that it is caused by central banks but by another factor. Demographics.

According to their theory, the demographic change, the aging society, pushes the natural rate of interest down. The natural rate of interest theory goes back to Swedish economist Knut Wicksell who formulated a thesis around the term natural interest (firstly used by Austrian economist Eugen von Böhm-Bawerk in his book Capital and Interest).

‘[The natural interest is a] certain rate of interest on loans which is neutral in respect to commodity prices and tends neither to raise nor to lower them’

- Knut Wicksell, Interst and Prices (1898) -

The natural interest cannot be observed, and it is a theoretical construct. Because Wicksell published his work in German, the theory got forgotten for several years (apart from the Austrian School) until economists included it into their IS-LM models (Laubach, 2006).

After the Great Financial Crisis of 2008, a discussion broke out if the fall in the interest rate level could be explained by a fall in the natural rate of interest and that central banks just followed natural forces and did not have a choice other than to lower the rate of interest to guarantee the optimum output potential for the economy.

Various traders, analysts, and economists argue that the aging of the society has resulted in more debt, less growth, and thus a fall in the equilibrium rate of interest.

The argument goes like this: total economic output is dependent on three factors, land, labor, and capital. Capital can help make labor more productive, and if the labor force declines, economic output also falls, ceteris paribus.

At the same time, aging societies have a lower level of income (pensions), and thus they consume less. Milton Friedman and Franco Modigliani (both Nobel laureates) talked about how people save less when young and old while building up a savings cushion during their work-life. However, people like Larry Summers argue that in an aging society, savings increase while demand is falling, and thus productivity and demand for investments lead to lower natural rates.

At first sight, the connection between demographics and interest rates seems obvious, as Chart 1 shows (it was shared various times on Twitter recently). It shows the 10y average annual labor force growth and the 20y US-treasury yield.

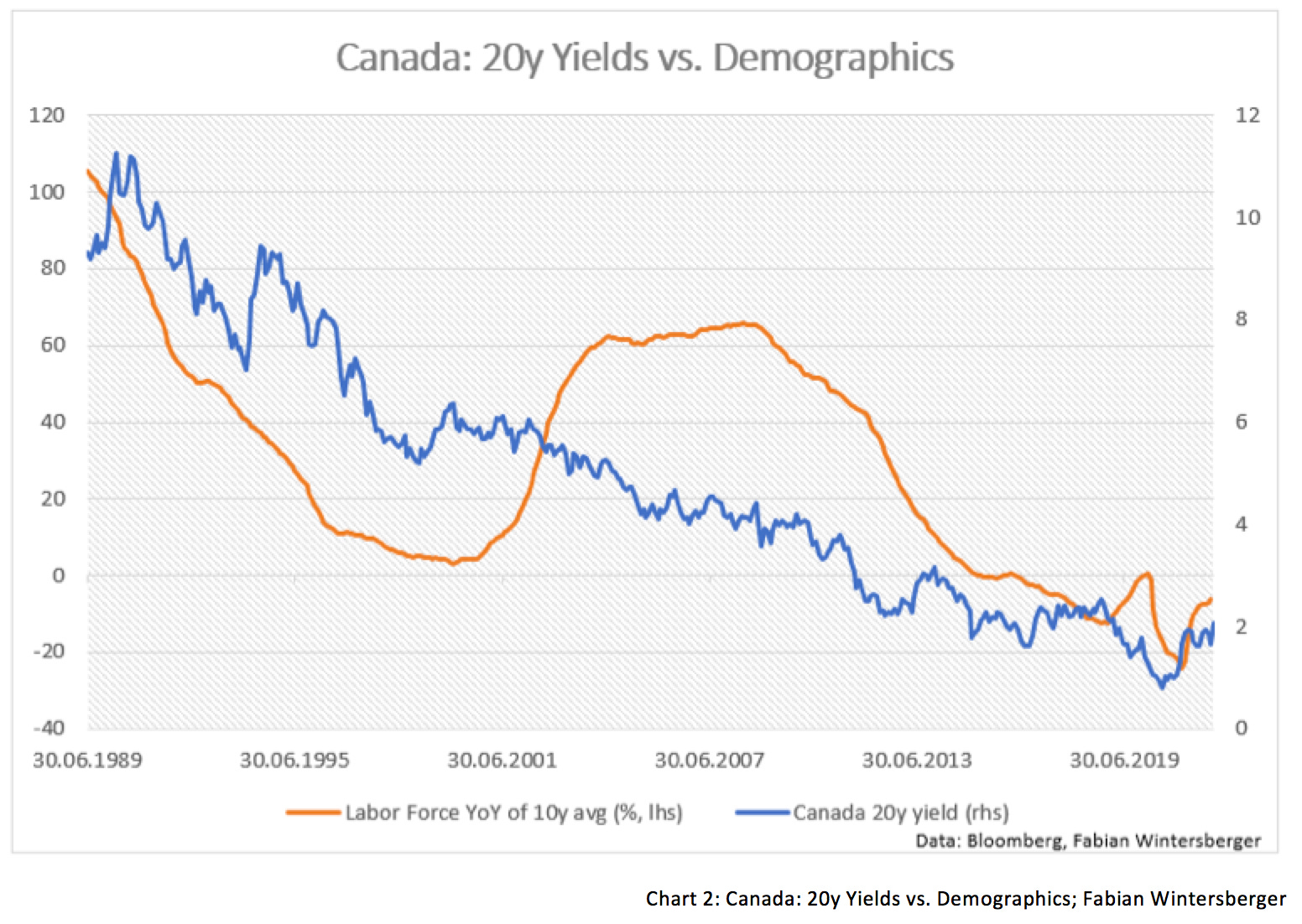

Is the connection as evident as the US example shows? Is correlation causality? In Chart 2, I do the same analysis for Canada (1989-today). While it suggests at least some connection, the correlation is much weaker than for the US.

If demographics is such an influential factor as everybody claims, rates in Canada should have risen between 2001 and 2008, or, at least, stay the same. But yields continued to fall.

For Italy, the picture is similar to the one in Chart 2. The causation is not as strong as the advocates of the theory suggest. Further, productivity per hour worked has increased enormously since 1980. Therefore we must conclude that the change in demographics did not primarily cause weaker economic growth. But more on that later.

Until now, I have illuminated the neoclassical, Keynesian argument, which tries to explain the current low-interest-rate environment. According to people like Larry Summers, the aging of the society caused the economy to fall into secular stagnation and the fall in the natural rate of interest (r*). Central banks policy only adjusted to the changing environment and will bring rates back up again if the circumstances change. But is the famous savings glut really a thing?

Now, let us examine the argument that there is a savings glut because of the change in demographics. According to the theory, the low interest rate environment has nothing to do with central banks. Rates are solely low because of the rise in savings available caused by aging societies.

German economists Gunther Schnabl (University of Leipzig) and Thomas Mayer (Flossbach von Storch Research) have tested the theory in a paper published last year. In the paper, they compared old-age dependency and household savings rates in OECD countries and found no correlation.

Thus, empirics do not support the savings glut theory. On the contrary, it may hint at the assumption that central banks may indeed be the primary driver of the fall in interest rates because they have pushed interest rates below the natural rate.

The same is true for the secular stagnation theory. As Schnabl and Mayer show, there is no fall in the marginal productivity of capital as suggested by the theory.

And there may be another problem with this theory: The model does not deal with the fact that loans are not made through savings but with newly created units of currency in our current financial systems. While loan growth to the real economy has faltered over the years, financial investment increased, and the reason behind that is artificially low interest rates.

That is why I think the argument that the change in demographics is the main reason behind low interest rates is wrong. Interestingly, a 2021 published paper by the Kansas-City Fed also dismisses the argument.

Addmidetely, the authors come to another conclusion: They claim that the real reason behind the current interest rate environment is rising inequality because wealthier households tendentially save more than poorer households. They suggest that increasing inequality has caused the savings glut.

Leaving aside the, as shown in Chart 3, a savings glut is not observable in the data. It seems that they put the cart before the horse there. I would argue in the opposite direction: artificially low interest rates have caused the rise in inequality because it has made it easier for wealthy households to accumulate assets compared to a higher interest rate environment.

Simultaneously, lower interest rates cause a rise in asset prices, and hence wealthy households enjoy paper gains in the assets they already possess. As a result, they have easier access to credit. Consequently, it is the other way: lower interest rates cause higher inequality.

The paper further argues that lower-income households would benefit from lower interest rates because they can borrow more. However, this counteracts the argument that higher savings from the wealthy lead to lower interest rates. If a rise in savings causes interest rates to fall, then a surge in loan growth would lead to rising interest rates.

Instead, central bank policy is a more plausible cause of the current economic environment. Let me briefly bring in the Austrian theory of interest, where (simplified) the interest rate represents a person’s time preference. People with a higher time preference prefer present consumption to future consumption and vice versa. But time preference cannot become negative. Or would you choose consumption in 30 years over current consumption?

Central banks have set the rate of interest below the level it would be in a free market where the rate is set by supply and demand, which has led to severe economic problems.

One point is that zero- and negative interest rate policies have provided a lifeline to unproductive businesses who can only stay within the market because of low rates. As those unproductive production facilities bind resources, they hamper economic growth, and that is why low-interest rates do not lead to a rise in productivity.

Further, keep in mind that a fall in interest rates (especially in longer-term interest rates) signals economic trouble ahead. Thus investors may push back on investing in the real economy (because they perceive it as a risk).

Banks hesitated to loan to businesses after the GFC in 2008 (especially in developed world economies), despite lower interest rates.

That is why the ECB and the Fed followed the Bank of Japan and introduced their versions of Quantitative Easing. The idea was that by buying assets (treasuries and MBS) from the banks, the banks’ balance sheets become more healthy, and due to the rise in bank reserves, it stimulates real economic activity (higher loan growth).

Now you may argue that additional government debt stimulated the real economy, which may be partly true. The fall in money velocity is a symptom of this development because the marginal productivity of debt has been falling for decades now. That is the Lacy Hunt argument. But it simply underlines the argument, that governments do not invest wisely.

And central banks know that QE does not lead to admired consequences. Still, they cannot admit that because it works in their econometric models (there is no input for money, and they are primarily based on inflation expectation theory). Jeff Snider (Alhambra Investments) recently put it very well (the whole interview is worth a watch):

‘They knew [QE] did’t not work in Japan… but it is just that the Japanese used it the wrong way…They just blow your mind how they say this does not work but then they come to the conclusion that it must work…they know that it does not work, but they keep on claiming: ‘QE did not fail we just cannot identify the benefits’… I am paraphrasing, but I am not paraphrasing that much’ - Jeff Snider

But still, central banks kept doing the wrong thing over and over again. If QE1 did not work, it was too little (according to them). Therefore, one needs to implement a new QE program on a bigger scale. And again, banks did not boost their lending into the real economy but bought treasury bonds because they knew they could sell them to central banks at a mark-up.

Because econometric models used by the central banks cannot reproduce economic reality, the admired effects just do not become a reality (hello, Eurodollar system!). It sounds astonishing that central banks keep doing the wrong thing because of their deepest beliefs that it will work the next time.

I have written on several occasions here (and here) that central banks are trapped. On the one hand, by keeping rates too low, they risk inflation getting out of hand (especially after the craziness of 2020 & 2021), and on the other hand, because with every increase in rates, they may cause the next recession. The rising involvement of governments in credit creation (via loan guarantees & stimulus checks) is a much more inflationary factor that will continue in the next years, whenever the system struggles.

Overall, central bank interventions did not make the system any better and did not make the system safer. I would argue that it has made the system even more fragile susceptible to crises (Butterfly-Effect), where even a little trouble can lead to enormous problems. Let me formulate it this way: The fear of short-term pain leads to the effect that central banks are risking the long-term health of the financial system.

This brings me back to A Little Piece Of Heaven by Avenged Sevenfold. Central banks (and governments) remind me of the protagonists in this song, as they try to subdue market forces by more and more interventionist policies.

But just as the female protagonist in A Little Piece Of Heaven, economic reality eventually kicks back, and at some point, it may lead to a ‘wedding’; the creation of a new financial system.

Whether this will be a heavily regulated or a free system is currently unknown. The same goes for the question of what the final nail in the coffin is: will it be an inflationary crack-up boom or a deflationary bust. Undoubtedly, both scenarios are somewhat suboptimal. Marc Farber once said that it is not about winning when a crisis hits. Everyone loses in a crisis, and the trick is to cut your losses as much as possible.

Have a great weekend!

Fabian Wintersberger

Thank you for reading! You can subscribe and get every post directly into your inbox if you like what I write. Also, it would be fantastic if you shared it on social media or liked the post! It’s just a click for you, but it would mean the world for me!

(All posts are my personal opinion only and do not represent those of people, institutions, or organizations that the owner may or may not be associated with in a professional or personal capacity.)